· 7 min read

You moved countries. You have income in two places, possibly assets in a third. You open a tax calculator, fill in your numbers, and get a figure back. It looks precise. It probably isn't.

The gap between what a calculator shows and what your tax office determines is rarely a data-entry error. It's the calculator itself - built for one country, one tax year, one set of rules. The moment your life crossed a border, the tool stopped working for you. It just didn't tell you that.

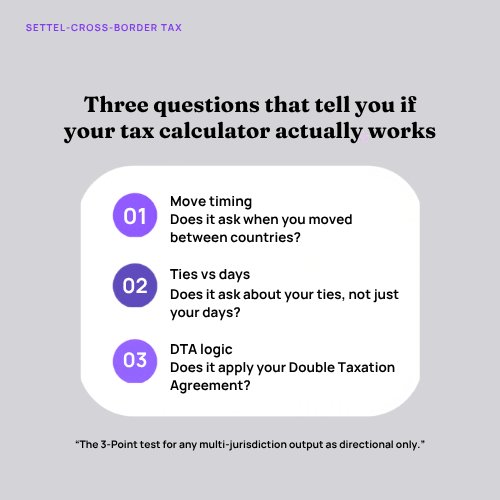

Three questions will tell you whether the tool you're using actually handles cross-border complexity - or is quietly simplifying it away.

Why Generic Calculators Fail Expats and Global Earners

Single-country tax calculators share three structural failure modes.

They assume your tax year matches the calendar year - it probably doesn't. They count days and ignore ties - the UK's Statutory Residence Test uses both. And they apply default withholding rates without checking whether a Double Taxation Agreement reduces what you actually owe.

Each failure mode can materially affect your tax position. Together, for someone managing the Three-Country Problem - living in one country, earning in another, holding assets in a third - they compound.

The three tests below tell you whether your calculator handles any of them.

Test 1 - Does It Ask When You Moved Between Countries?

This is the single most revealing question you can put to any multi-jurisdiction tax calculator.

Different countries run different tax years. The UK runs April to April. The US runs January to January. If you move between them mid-year, you don't have one tax year to manage. You have overlapping partial years, with different allowances, different rates, and different filing obligations in each.

Kiran is a UK-based software engineer who relocated from London to New York on 15 March 2026. His income for the year: £95,000 salary plus £8,000 in UK rental income that continued after he left.

A calculator that asks only "What is your income?" treats his year as a single block. In reality, Kiran has three distinct periods:

| Period | Jurisdiction | Status | What applies |

|---|---|---|---|

| Apr 2025 – Mar 2026 | UK tax year 2025/26 | UK resident for 11.5 months | UK income tax on earnings to date of departure; split-year treatment may apply if statutory conditions are met and correctly reflected in his Self Assessment return |

| Jan – Mar 2026 | US tax year 2026 (partial) | Becomes US resident from March | US Substantial Presence Test clock starts — a weighted multi-year day-count test based on presence over the current and prior two years |

| Apr 2026 onward | UK tax year 2026/27 | Status uncertain | SRT tie analysis required |

Split-year treatment - the UK mechanism that taxes only the portion of the year when you were actually resident - does not apply by default. It only applies if you meet specific statutory conditions and correctly reflect that treatment in your Self Assessment return. A calculator that doesn't ask your move date cannot begin to account for this.

A serious multi-country tax calculator must:

- Ask move-in and move-out dates for each country — not just which countries you're connected to

- Model overlapping tax years (for example, UK April–April versus US January–December) for the year of a move

- Hold at least two to three years of presence history, since tests like the US Substantial Presence Test are weighted across multiple years, not just the current one

- Identify whether split-year or part-year residency treatment applies under local law, and flag it — not assume it away

🚩 Red flag: The calculator assumes your tax year matches the calendar year, or doesn't ask when you moved. It's not built for cross-border complexity.

Test 2 - Does It Ask About Your Ties, Not Just Your Days?

The 183-day rule is the most widely cited threshold in expat tax. It's also, on its own, increasingly insufficient.

Modern residency tests look beyond physical presence to where your life actually centres. The UK's Statutory Residence Test (SRT) - published in full by HMRC - is the clearest example of this shift.

What the Statutory Residence Test is: A framework used by HMRC to determine whether an individual is UK-resident for tax purposes in a given tax year, based on a combination of days spent in the UK and specific ties to the UK - not days alone.

The five SRT ties:

| Tie | What it means | Threshold |

|---|---|---|

| Family tie | Spouse/civil partner or minor child is UK-resident (subject to HMRC carve-outs for children in full-time education) | Specific HMRC conditions apply |

| Accommodation tie | A UK home available to you where you spend at least one night — or at least 16 nights if it is a close relative's home | Available for 91+ days in the tax year |

| Work tie | Working in the UK (3+ hours counts as a work day) | 40+ work days |

| 90-day tie | Substantial prior presence in the UK | More than 90 days in either of the past two tax years |

| Country tie | Where you spend most of your time | More days in UK than in any other single country |

The number of ties you hold determines how many days you can spend in the UK before becoming resident - though the precise thresholds depend on whether you've been UK-resident in any of the previous three tax years. For recent leavers, more than 120 days in the UK with even one tie is generally enough to trigger UK residence under HMRC's sufficient-ties rules.

Priya moved from London to Dubai in 2024 but kept her London flat - available and used occasionally. She worked three days remotely for a UK client during visits. She spent 130 days in the UK in 2025/26 and assumed she was non-resident. She wasn't.

Her accommodation tie and work tie were both active. As a recent leaver spending more than 120 days in the UK, even one tie is enough for UK residence under HMRC's sufficient-ties rules. At 130 days with two ties, she's clearly resident. Her calculator - which only counted days - missed this entirely.

I moved between Kuwait, India, and the UK across different chapters of my career. Each time, the thing I trusted most - a tidy spreadsheet, a calculator, a rough count of days - was the thing most likely to be wrong. Not because the maths was bad, but because the model behind it wasn't built for a life that crossed borders. The day count was always the easy part. The ties were what caught people out, and they were invisible in every tool I tried.

A serious multi-country tax calculator must:

- Ask whether you have an available UK property, and how many nights you spend there

- Record UK workdays in the year, using the correct 3-hour threshold

- Check whether your spouse or children are UK-resident

- Use your day counts from the prior two tax years, not just the current one

- Distinguish between recent-leaver and arriver status - the day-count thresholds differ between the two

🚩 Red flag: The calculator asks only "How many days were you in the UK?" It's running an outdated model. Ties matter as much as days.

Test 3 - Does It Apply Your Double Taxation Agreement?

This is where multi-jurisdiction tax calculators most commonly fail in ways that cost people real money.

What a Double Taxation Agreement is: A treaty between two countries that determines which state has the right to tax specific types of income, and that often reduces withholding rates below the domestic default for eligible residents.

A DTA typically:

- Allocates taxing rights between two countries by income type

- Sets reduced withholding rates for dividends, interest, and royalties

- Includes tie-breaker rules for dual residents

- Requires an active claim - a form such as W-8BEN, or a declaration in your tax return — to take effect

Without DTA awareness, a calculator applies worst-case default rates. Those defaults are frequently not what a qualifying resident would actually owe.

Take the UK-US corridor. The US automatically withholds 30% tax on dividends paid to non-US residents. For a UK resident, that's the starting position. But under Article 10 of the US-UK Double Taxation Convention, portfolio investors who are UK-resident beneficial owners - holding less than 10% of any company - can reduce that rate to 15%, by filing a W-8BEN form through their broker.

The US withholds 30% on dividends by default. The US-UK treaty rate for qualifying UK residents is 15% on portfolio dividends. The difference does not come back automatically - you have to claim it.

Arun is a UK resident with £40,000 in US dividend income from a NASDAQ-listed portfolio where he holds less than 10% of any company.

| Scenario | Withholding rate | Tax withheld | Difference |

|---|---|---|---|

| Default (no treaty claim) | 30% | £12,000 | - |

| US-UK DTA rate (W-8BEN filed with broker) | 15% | £6,000 | £6,000 |

The £6,000 difference is not recovered automatically. It requires the right form, filed correctly, before the income is paid.

Two important caveats. First, the 15% rate applies to portfolio dividends where ownership is below 10%. Substantial shareholdings, pensions, interest, and royalties are handled differently under the treaty — each with its own provisions and claiming mechanism. Second, the W-8BEN approach works for most brokerage accounts; income received directly from a US payer or held in a wrapper may require a different process.

DTAs vary by country pair and by income type. The UK-India and UK-UAE corridors have their own treaty structures. What applies in the US-UK corridor doesn't automatically transfer elsewhere.

A serious multi-country tax calculator must:

- Identify the relevant Double Taxation Agreement for your specific corridor — not apply generic default rates across all countries

- Distinguish between income types: portfolio dividends, substantial shareholdings, pensions, employment income, interest, and royalties are not all treated the same under any treaty

- Show which treaty article was applied and what assumptions were made about beneficial ownership and thresholds

- Flag that treaty benefits require an active claim and are not applied automatically

🚩 Red flag: The calculator makes no mention of the relevant DTA for your corridor. It's applying worst-case default rates, not the treaty rates that may apply to your situation.

The 3-Point Checklist

| Test | What a basic calculator does | What an expat-grade engine must do |

|---|---|---|

| Move timing | Assumes one tax year; ignores move date | Asks move-in/out dates by country; models overlapping tax years and split-year treatment |

| Ties vs days | Counts days only | Asks about accommodation, work, family, and prior presence; applies sufficient-ties rules by leaver/arriver status |

| DTA logic | Applies default withholding rates | Identifies the treaty for your corridor; distinguishes income types; shows which article applies |

If your current calculator fails any of these tests, treat its output as directional only. For decisions about where to live, how to hold assets, or when to move, directional is not enough.

In short: a reliable multi-country tax calculator for expats and global earners must do three things - track exact move dates and overlapping tax years, combine day counts with residency ties such as family, accommodation, and prior presence, and apply the correct tax treaty and withholding rate to each income stream for each corridor.

What Settel Does Differently

Settel is built for the Three-Country Problem - the situation where you live in one country, earn in another, and hold assets in a third. Standard tools assume a single-country life. Settel doesn't.

The Smart Tax Engine maps directly to all three tests. It models overlapping tax years and move dates, not just annual totals. The day-count tracker monitors your SRT tie thresholds in real time — not just total days in a country, but which ties are active and how many days remain before your status changes. Treaty logic is applied per corridor, with transparent assumptions about income type and beneficial ownership.

Coming soon: Settel AI - an LLM-powered feature that will help you understand your full cross-border tax and wealth position, surface treaty provisions relevant to your corridors, and identify the questions worth taking to your tax adviser. It explains why a given residency or treaty outcome appears in your numbers. It does not replace the adviser.

We don't provide tax advice. We show you the maths. You know what to do.

You're earning across borders, probably holding assets in more than one country, and doing this research yourself because no tool you've found has actually been built for your situation. That's the gap Settel closes. Put your numbers in once. See your actual position - move dates, ties, treaty rates - not a single-country approximation of it. app.settel.io

Informational only — not financial advice. Settel is a tracking and calculation tool. Always consult a qualified tax professional for advice specific to your situation.

When You Still Need a Tax Adviser

No calculator -including Settel - fully resolves every cross-border situation. Some scenarios require professional judgement that software cannot substitute for.

These include: deemed domicile and the remittance basis for long-term UK residents; RNOR (Resident but Not Ordinarily Resident) status on return to India; social security totalisation agreements; complex carried-interest or partnership structures; citizenship-linked obligations, particularly for US citizens living abroad who file a US return regardless of residence; and any situation where two countries claim primary taxing rights without a DTA tie-breaker to resolve the conflict.

Use a calculator for scenario testing, early planning, and preparation for your professional consultation. Use an adviser for the decisions.

Frequently Asked Questions

How accurate are expat tax calculators?

It depends entirely on what the calculator was built to handle - and most weren't built for your situation. A single-country tool applied to a multi-country life produces confident-looking numbers that can be significantly wrong, not because you entered anything incorrectly, but because the model behind it doesn't account for split tax years, residency ties, or treaty withholding rates. Run the 3-point test above before you trust any output.

Do tax calculators handle double taxation agreements?

Most don't - or handle them incompletely. A DTA-aware calculator must identify the specific treaty for your corridor, distinguish between income types (portfolio dividends, pensions, employment income, and royalties are all treated differently), and apply the correct article-level rate. It must also flag that treaty benefits require an active claim - a W-8BEN through your broker, or a declaration in your return - and are not applied automatically. If your calculator doesn't surface the relevant treaty for your corridor, it's applying default rates.

Can I be tax-resident in two countries at the same time?

Yes, and it's more common than most people expect. If you meet each country's residency test independently — the UK Statutory Residence Test, the US Substantial Presence Test, or another country's equivalent - you can be dual-resident simultaneously. Most Double Taxation Agreements include tie-breaker rules (permanent home, centre of vital interests, habitual abode) to determine which country gets primary taxing rights. Where no DTA exists, sustained double taxation is a genuine risk. Get qualified advice specific to your corridor.

What is the Three-Country Problem?

The Three-Country Problem is what happens when you earn income in one country, live in a second, and retain tax obligations - through citizenship, property, or prior residency - in a third. Each country applies its own rules, its own tax year, and its own residency test. Standard calculators produce estimates based on a single-country life that no longer describes your situation. The problem is not complexity for its own sake - it's that the tools most people reach for were never designed for it.

Can a multi-jurisdiction tax calculator replace a tax adviser?

No. A well-built multi-country tax calculator gives you accurate scenario modelling, residency threshold monitoring, and treaty-aware calculations for your corridors. What it cannot do is apply professional judgement to edge cases: deemed domicile, RNOR status, citizenship-based filing obligations, or situations where two countries claim taxing rights without a clear treaty resolution. Use the calculator to understand your position and prepare the right questions. Use the adviser to answer them.

Informational only - not financial advice. Settel is a tracking and calculation tool. Tax laws and treaty interpretations change; examples in this post are simplified and omit nuances including non-dom status, remittance basis, and citizenship-linked tax obligations. Always consult a qualified tax professional for advice specific to your situation.