· 12 min read

Who This Guide Is For

Most expats I know find out they owe tax in a second country not from a tax adviser - but from a letter they weren't expecting. By then the deadline has usually passed. This guide exists so that doesn't happen to you.

It's for expats, digital nomads, globally mobile professionals, NRIs, NRAs, and multi-currency earners managing finances across the UK, US, India, and UAE - particularly anyone facing what we call the Three-Country Problem. If your income, assets, or residency spans more than one of these corridors - UK-India, UK-UAE, UK-US, India-UAE, India-US, US-UAE - this guide works through the full calculation chain step by step.

TL;DR - Global Expat Tax in 2026

The Three-Country Problem is what happens when you earn in one country, live in another, and have assets in a third - and all three tax systems have a legitimate claim on you at the same time. I built Settel because I lived this. The rules don't overlap cleanly. Neither do the deadlines.

- Residency first. Each country applies its own test. "Under 183 days" does not mean non-resident anywhere - the UK SRT ties matrix and India's 120-day rule both catch people well below that threshold.

- Treaties allocate, not eliminate. DTAs determine which country taxes which income type. They do not automatically exempt you. Credits do the work of preventing double taxation - but you must claim them.

- Credits require forms and deadlines. UK (SA106), US (Form 1116), India (Form 67 / Form 44). Miss the deadline, lose the credit.

- FX method must be consistent. Choose transaction-date or annual-average rates and apply one method throughout each return.

- Deadlines differ by corridor. US: April 15 (June 15 automatic for expats). UK: 31 January 2027 (2025-26). India: verify CBDT deadline before filing each year.

Quick Decision Flow - Where Do I Owe Tax as an Expat?

- Determine your tax residency in each country (UK SRT, India Section 6, US substantial presence test, UAE visa status).

- List all income by country of source - where the work is done or the asset is located.

- Check which double taxation agreement applies for each income type and corridor.

- Calculate foreign tax paid at source.

- Apply foreign tax credits in your country of residence, using the correct form by the correct deadline.

- Convert all figures into your filing currency using your chosen, officially permitted FX method - applied consistently.

Global Expat Tax Checklist for 2026 (UK, US, India, UAE)

| # | Action | Why it matters |

|---|---|---|

| 1 | Determine residency status in every country where you have income or assets | Residency determines whether worldwide or source-only income is taxable there |

| 2 | Apply ties test / Section 6 / SPT - not just the day count | The simple day count is only the automatic test; the ties rules and 120-day rule catch many expats |

| 3 | Identify treaty for each income type per corridor | Different articles apply to salary, dividends, capital gains, and rental income |

| 4 | Calculate foreign tax paid with official documentation | Withholding certificates required - bank statements are not sufficient |

| 5 | File foreign tax credit form before the deadline | UK: SA106 by 31 Jan; US: Form 1116 with return; India: Form 67 / Form 44 by end of AY |

| 6 | Fix your FX rate method for the whole return | Inconsistency within a single return is an audit flag |

| 7 | Verify filing deadlines for the current year | CBDT extends Indian deadlines annually; do not assume 31 July |

Where Expats Most Often Overpay Tax by Corridor

| Corridor | Common mistake | What to do instead |

|---|---|---|

| UK–India | Assuming DTAA exempts Indian mutual fund gains from UK CGT | Both countries tax; claim UK FTCR for Indian tax paid (SA106) |

| UK–US | Treating RSU vesting as capital gains, not employment income | Apply Article 15 (employment); credit US withholding against UK PAYE |

| India–UAE | Assuming UAE residency automatically breaks Indian residency | India's 120-day rule and deemed residency provision apply regardless of UAE tax status |

| US–India | Missing Form 1116 passive basket rules on Indian dividends | Categorise correctly; excess credits carry forward 10 years in the US |

| UK–UAE | Not tracking UK ties after leaving for Dubai | Leaver with 3 ties is UK-resident at 46 days - keep travel records |

| US–UAE | US citizens assuming UAE exempts them from US filing | US citizens file worldwide regardless of residency |

Step 1 - Why Global Expat Tax Is Multi-Step, Not Single-Jurisdiction

Most globally mobile professionals underestimate how many separate calculations sit between "I earned income in two countries" and "I know what I owe and where." Getting your global tax obligations right requires five distinct steps - each of which feeds the next, and each of which can fail independently.

Before the arithmetic, five terms structure everything that follows:

Residency - which country can tax your worldwide income. Determined by each jurisdiction independently, using its own tests.

Source - where specific income originates. Employment income is typically sourced where the work is performed. Investment income is sourced where the asset or entity is located.

DTAA allocation - which country taxes which income when residency and source sit in different jurisdictions. Set by the relevant bilateral treaty, not by either country acting alone.

Foreign tax credit - the mechanism in your residence country that prevents you being taxed twice in full on income already taxed at source.

FX reporting - the conversion of foreign income and gains into your filing currency, using the rate methodology required by your residence country's tax authority.

Misclassifying at any step cascades forward. A wrong residency determination produces a wrong source analysis, which produces a wrong treaty application, which produces a wrong credit calculation. The chain is sequential. The starting point is always residency.

See how these errors compound in practice: fixing multi-country tax calculator errors before HMRC does.

Quick answer: Do I owe tax in every country I have income from?

Not necessarily. Residency determines whether a country can tax your worldwide income or only income sourced within its borders. Source rules determine which income is taxable in non-resident countries. Treaties then allocate those rights between countries and set limits on withholding. You may have filing obligations without having a net tax liability - but the filing obligation exists independently.

Step 2 - Map Your Expat Tax Residency: UK, US, India, UAE

United Kingdom - Statutory Residence Test

The UK Statutory Residence Test (SRT) works in three layers. You first check the automatic overseas tests (non-residence if you spend fewer than 16 days in the UK and were previously resident, or fewer than 46 days and were not). If those do not apply, you check the automatic UK tests. Spending 183 or more UK days in the tax year makes you automatically resident - no further analysis needed.

Below 183 days, you are not automatically non-resident. The sufficient ties test applies. Five possible ties: family (UK-resident spouse, civil partner, or minor children), accommodation (UK accommodation available for 91+ consecutive days, used at least once), work (40+ UK workdays of at least three hours), a 90-day tie (more than 90 UK days in either of the previous two tax years), and a country tie (UK is where you spend the most days - leavers only).

The day-count thresholds under the sufficient ties test:

| Status | Ties held | UK-resident if UK days exceed |

|---|---|---|

| Leaver (previously UK-resident) | 1 | 182 |

| Leaver | 2 | 90 |

| Leaver | 3 | 45 |

| Leaver | 4 or 5 | 15 |

| Arriver (not previously UK-resident) | 2 | 120 |

| Arriver | 3 | 90 |

| Arriver | 4 | 45 |

Source: Stephenson Harwood SRT Overview, 2025

A leaver with 3 ties is UK-resident at 46 UK days. An arriver with 2 ties is UK-resident at 121 UK days. The simplified 183-day rule is only the automatic test - it is not a ceiling for leavers with ties.

For detailed UK residency rules and how they interact with expat income, see Settel's UK expat tax guide.

Quick answer: Can I be UK-resident even if I spend fewer than 183 days in the UK?

Yes. If you were UK-resident in any of the previous three tax years (a "leaver"), the sufficient ties test applies. With three UK ties, you become UK-resident at just 46 days. With four or five ties, at 15 days. Day count alone does not determine UK residency for leavers.

India - Three Residency Tests for Expats, Not One

India's Section 6 of the Income Tax Act, 1961 contains three separate residency tests for individuals.

Test 1 - 182-day rule: Present in India for 182 days or more in the financial year.

Test 2 - 60 days + 365 days: Present for 60 days or more in the current year, plus 365 days or more across the four preceding years. Both conditions must be met.

Test 3 - 120-day rule (Finance Act 2020): Applies only to visiting Indian citizens and persons of Indian origin (PIOs) whose Indian-source income (excluding foreign income) exceeds ₹15 lakh in the relevant year. For that group, 120 days in India plus the 365-days-in-4-years condition triggers resident status.

Mini-case: the 120-day rule in action

Priya is an Indian citizen based in Dubai. Her Indian-source income (rental, dividends) is ₹18 lakh for FY 2025-26. She spent 125 days in India this year. Under the standard 182-day rule she is non-resident. Under the 120-day rule she is not - 125 days plus ₹18 lakh Indian income means she meets the test and is classified as resident. Because she has been NRI for more than 9 of the past 10 years, she qualifies as RNOR (Resident but Not Ordinarily Resident). Her foreign income remains outside India's tax net during the RNOR period. Her Indian-source income is taxable in India.

If her Indian-source income were ₹12 lakh, the 120-day rule would not apply. She would need 182 days to become resident. At 125 days she would remain NRI.

RNOR status sits between NRI and full resident. It applies when a returning NRI has been non-resident for 9 of the preceding 10 years, or spent 729 days or fewer in India over the preceding 7 years. RNOR individuals are taxed on Indian-source income but not on foreign income - unless the foreign income arises from a business controlled from India. It is a time-limited window. Understand when yours closes.

The RNOR window is one of the things I see misunderstood most consistently - both in Settel user data and in conversations with returning NRIs before that. People know they have a transitional period, but they don't track when it closes, and they don't plan around the year it does. That final year - when you shift from RNOR to fully ordinarily resident - is the one that tends to produce the largest unexpected Indian tax bill.

For NRI and RNOR residency rules in full, see Settel's India NRI tax guide.

Quick answer: Does the 120-day rule apply to all NRIs visiting India?

No. It applies only to visiting Indian citizens and PIOs whose Indian-source income (excluding foreign earnings) exceeds ₹15 lakh in the relevant financial year. Below that income threshold, the standard 182-day rule applies. The threshold is Indian-source income specifically - foreign salary and overseas investment income do not count towards it.

United States - Substantial Presence Test

For non-citizens without a green card, the US applies the substantial presence test. Two conditions must both be met: at least 31 days in the US in the current year, and 183 or more weighted days across three years using this formula:

All current-year days × 1 + prior-year days × ⅓ + two-years-prior days × ⅙

Worked example: 150 current-year days, 90 prior-year days, 60 two-years-prior days.

150 + (90 × ⅓) + (60 × ⅙) = 150 + 30 + 10 = 190 days → US tax resident

Green card holders are automatically US tax residents regardless of days. US citizens are taxed on worldwide income regardless of residency or location.

Source: IRS Substantial Presence Test

For US expat filing obligations, see Settel's US expat tax guide.

UAE - Residency for Treaty Purposes

The UAE levies no personal income tax on employment income. UAE residence visa holders can claim UAE tax residency for treaty purposes. This matters primarily for establishing non-residence in other jurisdictions - but the UK SRT and India's tests determine whether you remain resident there regardless of UAE status.

When expat residency overlaps

Dual residence is common. Most DTAs between the UK, US, India, and UAE contain tie-breaker rules that resolve the conflict in sequence: permanent home available, centre of vital interests, habitual abode, nationality, competent authority determination. The tie-breaker assigns treaty-purpose residency to one country - domestic law filing obligations remain.

Step 3 - DTAA Allocation: Which Country Taxes Which Expat Income

Double taxation agreements do not eliminate tax. They allocate taxing rights by income type and resolve residency conflicts through tie-breakers.

Quick answer: Does a double tax treaty mean I pay tax in only one country?

Not always. Many treaties coordinate by credit rather than by exemption - both countries tax, but the residence country credits the tax already paid at source, capped at its own tax on that income. The treaty prevents full double taxation, not all double taxation. The credit is not automatic - you must claim it on the correct form by the correct deadline.

Corridor Case A - UK-India: Equity Mutual Fund Gains

Rohan is UK-resident under the SRT. He holds Indian equity mutual funds and redeems them in FY 2025-26, realising a long-term gain of ₹10 lakh (held more than 12 months).

Indian tax: LTCG on equity-oriented funds at 12.5% on gains exceeding the ₹1.25 lakh annual exemption. Taxable gain: ₹8.75 lakh. Indian tax: ₹8.75 lakh × 12.5% = approximately ₹1.09 lakh (before surcharge and cess).

Sources: Finance (No. 2) Act 2024, effective 23 July 2024; Budget 2026 confirmed no change to these rates

UK tax: Under Article 13 of the UK-India DTA (1993, as amended by 2013 Protocol), India - as the source country - has taxing rights on gains from Indian-source assets. The UK also taxes Rohan on those gains as a UK resident. The DTA coordinates by credit: India taxes first, the UK provides credit relief for Indian tax paid, capped at the lower of Indian tax paid or UK CGT on that gain.

Common expat mistake on this corridor: Assuming the DTAA exempts the gain from UK CGT entirely. It does not. Both countries tax. The credit is the mechanism that prevents full double taxation. An expat who does not file SA106 pays twice in full.

Corridor Case B - UK-US: RSU Vesting

Sarah is a UK-resident US citizen. Her US employer's RSUs vest while she is working in London. RSU vesting creates employment income - not capital gains - at the fair market value on the vest date.

The UK-US DTA allocates employment income to the country where the work is performed. Services performed in the UK are taxed in the UK as employment income. The US also taxes worldwide income of its citizens. Both countries tax the RSU income, coordinated by credit. The US provides a foreign tax credit (Form 1116) for UK income tax paid. The UK provides FTCR for any US withholding, capped per the lower-of rule.

Common expat mistake on this corridor: Treating RSU vesting as a capital gain. Wrong article, wrong rate, wrong credit calculation - and potentially a late PAYE assessment from HMRC.

The Core Principle for Expats

Each income type has its own treaty article. Employment income, dividends, interest, royalties, capital gains, and immovable property income are all treated differently. Applying the wrong article misstates taxing rights and withholding rates. Always check the specific article for your specific income type in the applicable treaty.

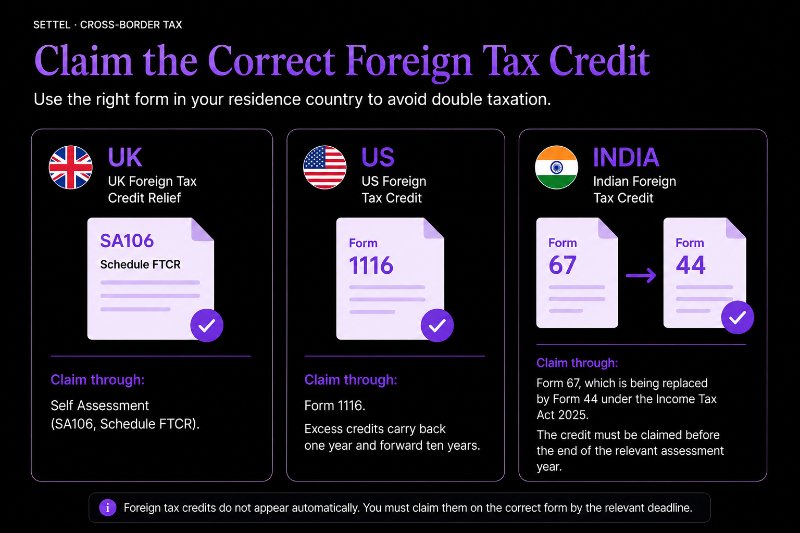

Step 4 - Foreign Tax Credits for Expats: The Arithmetic That Prevents Double Taxation

Once treaty allocation is clear, the foreign tax credit is the mechanism that prevents your residence country from taxing the same income in full again.

Quick answer: How do I make sure I don't pay tax twice on the same income?

Claim the foreign tax credit on the correct form in your residence country, for the tax paid at source, by the relevant deadline. The credit is capped at the lower of: foreign tax paid, or residence country tax on that same income. It does not appear automatically. An unclaimed credit means full double taxation on that income.

The Cap Calculation - Worked Example

Total UK income: £100,000. Of that, £30,000 is from Indian mutual funds on which approximately £1,000 of Indian tax has been paid.

Step 1: UK tax on total income (simplified, basic rate): £100,000 × 20% = £20,000.

Step 2: UK tax on income excluding the Indian gains: £70,000 × 20% = £14,000.

Step 3: UK tax attributable to the Indian gains: £20,000 − £14,000 = £6,000.

Maximum credit: lower of Indian tax paid (£1,000) and UK tax on that gain (£6,000) = £1,000 credit. UK net tax on the gains: £6,000 − £1,000 = £5,000.

The credit eliminates the Indian tax from the UK liability entirely in this case - because the Indian rate (12.5%) is lower than the UK rate (20%). Rohan does not pay double tax. He pays the higher of the two rates, once.

UK Foreign Tax Credit Relief

Claimed through Self Assessment (SA106, Schedule FTCR). Capped at the lower of: foreign tax paid or UK tax on that income. Excess credits cannot be carried forward for individuals. Timing matters - if Indian tax is paid in a different period from when the UK taxes the income, planning is needed.

Source: HMRC HS263 - Relief for Foreign Tax Paid

US Foreign Tax Credit - Form 1116

Dollar-for-dollar offset against US tax on foreign-source income, up to the US tax on that income. Excess credits carry back one year and forward ten years - a significant advantage over the UK system. Income must be correctly categorised between passive and general baskets before the credit is applied.

India - Form 67 (Becoming Form 44 Under Income Tax Act 2025)

For Indian residents with foreign income, the foreign tax credit is claimed through Form 67, which is being replaced by Form 44 under the Income Tax Act 2025. The credit must be claimed before the end of the relevant assessment year - for FY 2024-25 income, the deadline was 31 March 2026. The credit equals the lower of: foreign tax paid (converted to INR at the TT buying rate on the date of payment) or Indian tax on that same income. Excess credits do not carry forward in India - they lapse.

Source: Income Tax India - Form 67 guidance; India Briefing - Form 67 deadline

For a full walkthrough of foreign tax credit mechanics by corridor, see Settel's tax guides.

Step 5 - Multi-Currency FX for Expats: A Four-Step Workflow

FX conversion is where multi-jurisdiction expat filing goes quietly wrong. The obligation is simple - report in your filing currency - but the permitted rate methodology differs by country, and inconsistency within a single return is an audit flag.

Step 1 - Choose your method and fix it for the whole return. The IRS permits yearly average rates for most items; specific transaction rates for individual disposals. HMRC permits either transaction-date rates or annual average rates - applied consistently throughout the return.

Official rate sources: IRS yearly average exchange rates; HMRC exchange rate tables.

Step 2 - Apply the correct rate to each income type. Regular income (salary, interest, dividends): annual average is generally simplest. Individual disposals (property, share sales): transaction-date rate is typically most defensible. Indian FTC claims: convert foreign tax to INR at the TT buying rate on the date of payment (Rule 128 requirement).

Step 3 - Identify FX gains and losses. Foreign currency can itself be a taxable asset. A USD account held by a UK-resident expat: if $100,000 opened at a rate of 1.25 (£80,000 equivalent) and the rate moved to 1.30 by year end ($100,000 = £76,923), that is a reportable FX loss. Gains and losses on personal foreign currency are capital in nature. Keep records.

Step 4 - Crypto disposals require per-transaction FX. Every crypto-to-crypto trade is a disposal under UK CGT rules and US tax rules. Each trade requires FX conversion at transaction time, not at year end. Settel's multi-currency dashboard aggregates transactions across currencies and assets with real-time FX conversions, maintaining tax-accurate records throughout the year.

Quick answer: Which exchange rate should I use for my UK tax return?

HMRC permits either transaction-date rates or annual average rates, applied consistently for the whole return. The official source is HMRC's published exchange rate tables. Using rates from unspecified online sources without documentation creates compliance risk, and mixing methods within a return is a common audit flag.

Step 6 - Expat Tax Filing Deadlines and Penalties by Country

The decision tree: resident in this country → file a full return. Non-resident with local-source income → file a non-resident return or allow withholding at source. Non-resident UK landlord → HMRC Non-Resident Landlord Scheme applies.

Current filing deadlines (verify before filing - deadlines are subject to extension):

| Country | Current Deadline | Notes |

|---|---|---|

| United States | April 15 | Automatic extension to June 15 for expats with foreign tax home (no form; attach statement). Further extension to October 15 via Form 4868 (file by April 15). Tax owed accrues interest from April 15 regardless of filing extension. (IRS Publication 54) |

| United Kingdom | 31 January 2027 (2025-26 online) | Paper deadline: 31 October 2026. The 2024-25 online deadline (31 January 2026) has passed; late filing penalties now apply. (HMRC Self Assessment) |

| India | 16 September 2025 (AY 2025-26, CBDT extension) | Standard deadline is 31 July. Verify AY 2026-27 deadline with CBDT before filing - extensions are issued annually. (Income Tax India) |

| UAE | No personal income tax filing for employment income | - |

Penalty shocks - what non-compliance costs expats:

| Country | Late filing | Late payment |

|---|---|---|

| US | 5% per month on unpaid tax, up to 25% | 0.5% per month; interest from April 15 |

| UK | £100 immediate; escalates with time | Interest on unpaid tax |

| India | Section 234F fee up to ₹10,000; Section 234A/B/C interest | Interest from April 1 |

A zero-tax outcome after credits does not eliminate filing obligations or late-filing penalties. The obligation exists independently of whether tax is owed.

Step 7 - The Three-Country Scenario: Rohan's Numbers

Tier 2 scenario. UK-resident Indian citizen. UK employment income and Indian equity mutual fund gains. 118 days in India this year.

Parameters:

- UK salary: £80,000

- Indian equity mutual fund gain (LTCG, held >12 months): ₹10 lakh

- Days in India: 118

- Indian-source income: below ₹15 lakh - standard 182-day rule applies. Rohan should verify his exact Indian-source income total with a qualified adviser - the margin is narrow.

Step 1 - Residency. UK-resident under the SRT (leaver, multiple ties, well above the 45-day threshold with 3 ties). India: non-resident at 118 days under the 182-day standard rule, assuming Indian-source income is below ₹15 lakh.

Step 2 - Treaty allocation. Indian mutual fund gains are India-sourced. Under Article 13 of the UK-India DTA, India has taxing rights as source country. The UK also taxes as residence country, coordinated by credit.

Step 3 - Indian tax. LTCG on equity mutual funds: 12.5% on ₹8.75 lakh (₹10 lakh minus ₹1.25 lakh exemption) = approximately ₹1.09 lakh before surcharge and cess.

Step 4 - UK CGT. ₹10 lakh converts to approximately £9,200 at a mid-range rate. UK CGT applies after the annual exempt amount. At the basic rate (10% on capital gains if total income stays in the basic rate band), UK CGT on the gain is approximately £920. The £1,000 FTCR credit from Indian tax paid eliminates the UK CGT liability on this gain entirely. At the higher rate (20%), UK CGT is approximately £1,840; the credit reduces it to approximately £840. Rohan does not pay double tax on these gains either way.

Step 5 - File. India ITR (non-resident return) by the CBDT deadline for AY 2026-27 (verify before filing). UK Self Assessment by 31 January 2027 for 2025-26. Include SA106 with FTCR claim.

What if Indian-source income were ₹18 lakh and days 125? The 120-day rule triggers - Priya's scenario. Resident status applies, but likely RNOR given NRI history. The RNOR benefit: UK salary is not taxable in India if earned entirely from UK employment. Indian mutual fund gains remain taxable in India. The DTA credit mechanism still applies. But filing obligations, forms, and credit mechanics all shift. RNOR is a transitional status with a finite window - plan around it before it closes.

Common Expat Tax Pitfalls by Country

| Country | Typical expat mistake | Consequence | How to fix |

|---|---|---|---|

| UK | Assuming fewer than 183 days = non-resident | UK-resident as leaver with 3+ ties at 46 days; unexpected worldwide income exposure | Map ties before the year starts; track midnights |

| India | Ignoring the 120-day rule for Indian citizens/PIOs | Inadvertent resident status; Indian tax on worldwide income | Track Indian-source income separately from foreign income |

| US | Missing Form 1116 passive basket rules | Excess credits wasted; double tax on Indian or UK passive income | Categorise income by basket before filing; carryforward unused credits |

| UAE | Treating UAE residency as automatic tax exit from UK/India | UK SRT and India Section 6 still apply; dual-residence risk | Formally break residency in prior country under its own rules |

| All | Not filing a credit form because "no tax is owed" | Late filing penalties in all jurisdictions; credit deadline may lapse | File on time even when credits eliminate the liability |

How Settel Fits Into This Workflow

Settel is a multi-currency wealth and tax tracking platform for expats, digital nomads, and global professionals managing finances across the UK, US, India, and UAE. It is a tracking and calculation tool - not a tax adviser. It does not give regulated financial or tax advice and is outside the FCA perimeter.

The five steps above involve three types of hard problems: tracking the facts (days, income, FX rates, deadlines), applying the rules (residency tests, treaty provisions, credit caps), and filing correctly (right forms, right figures, right timing). Settel handles the first two.

Residency-aware day-count tracker: Monitors your physical presence against the UK SRT ties matrix (including leaver and arriver thresholds), India's 182-day and 120-day rules, and the US substantial presence test - in real time, before you cross a threshold rather than after. Alerts are keyed to your specific corridor and tie profile.

Multi-currency dashboard with separate tax-accurate FX per jurisdiction: Tracks your global net worth across currencies at official-source rates and maintains separate tax-accurate figures per filing jurisdiction, so the number you report in your UK Self Assessment and the number in your Indian ITR are both correct - and both traceable to a documented rate source.

Settel AI - will surface optimisation options across your full multi-jurisdiction position and explain the interaction between rules in plain language.

For deep technical guidance on your specific position, work with a specialist in cross-border taxation alongside Settel's numbers. For supporting detail on individual components of this workflow: UK expat tax rules · India NRI and RNOR guide · US expat tax obligations · UAE expat tax overview · All tax guides

If you've read this far, you're probably someone who earns in one country, holds assets in another, and lives somewhere in between - and you're tired of reconstructing your financial picture from three different spreadsheets every year. Settel won't replace your tax adviser, and it won't file your returns. What it will do is make sure the numbers going into that process are accurate, consistent, and already converted into the right currency at the right rate - before deadline pressure sets in. Start free at app.settel.io.

FAQ

How do I know which countries I need to file a tax return in as an expat?

Start with residency. Tax-resident in a country means you must file there and report worldwide income, subject to treaty exemptions. If you have income sourced in a country where you are not resident - rental income, capital gains on local assets, employment income from local work - that country may also require a filing or withhold at source. Most expats with income in two or more of the UK, US, India, and UAE have filing obligations in more than one jurisdiction simultaneously. The starting point is always a formal residency determination for each country, not a day count.

What happens if two countries both tax the same income?

That is what double taxation agreements are designed to prevent. The DTA allocates primary taxing rights based on where income is sourced and where you are resident. The residence country then grants a credit for tax already paid at source - capped at the residence country's tax on that same income. Without claiming the credit on the correct form by the correct deadline, you pay full tax in both countries. The treaty does not act automatically.

Does moving to the UAE mean I stop owing tax in the UK or India?

Not automatically. The UAE taxes no employment income, but it does not switch off your obligations elsewhere. The UK SRT and India's Section 6 both apply based on your own facts - days present, ties held, Indian-source income. Dual residence is a real outcome for UK-UAE and India-UAE expats, not an edge case. Formally break residency under each country's own rules; UAE status does not do that for you.

What is RNOR and does it apply to me?

RNOR - Resident but Not Ordinarily Resident - is a transitional status for returning NRIs who meet India's residency tests but have been non-resident for 9 of the preceding 10 years (or spent 729 days or fewer in India over the prior 7). While it applies, your foreign income stays outside India's tax net; Indian-source income is taxable. It has a fixed end date - when the window closes, your full worldwide income becomes taxable in India. Work out when yours closes before it does.

Informational only - not financial advice. Settel is a tracking and calculation tool. Always consult a qualified tax professional for advice specific to your situation.