You are probably paying tax in the wrong country. Or you think you are not paying tax somewhere you absolutely should be. Either way, you are guessing - and the guess is costing you.

I built Settel because I lived this. Kuwait, then India, then the UK, and at every move a different accountant telling me something different, none of them talking to each other, all of them billing me to reconstruct the same picture from scratch. Meanwhile, real obligations were quietly accumulating - FBAR deadlines I had never heard of, treaty credits nobody claimed on my behalf, a residency status I assumed was fine because I hadn't been questioned on it. The problem is not that the rules are complicated. The problem is that they sit across three different tax systems that were each designed as if the other two don't exist. And they don't care that you're busy.

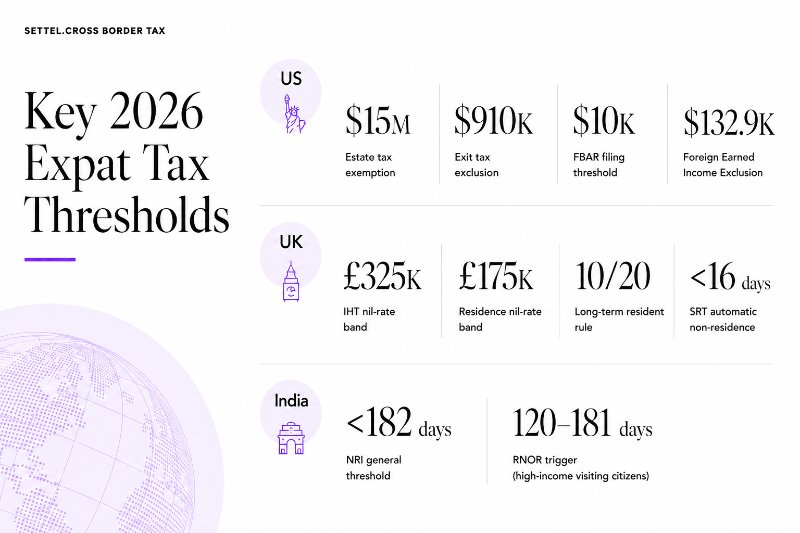

Quick Summary: Key 2026 Thresholds for Expats

| Jurisdiction | Item | 2026 Threshold / Rule |

|---|---|---|

| US | Federal estate tax exemption | $15,000,000 per individual ($30m per couple) - (IRS) |

| US | Exit tax exclusion (IRC §877A) | $910,000 of deemed gain - inflation-indexed annually - (IRS) |

| US | FBAR filing threshold | $10,000 aggregate foreign accounts at any point in calendar year - (IRS) |

| US | Foreign Earned Income Exclusion | $132,900 for tax year 2026 |

| UK | IHT nil-rate band (NRB) | £325,000 per individual (frozen to 2030-31) - (HMRC) |

| UK | IHT residence nil-rate band (RNRB) | £175,000 additional when home passes to direct descendants |

| UK | IHT long-term resident trigger | 10 of last 20 UK tax years → worldwide assets in scope at 40% - (HMRC) |

| UK | SRT automatic non-residence | Fewer than 16 UK days (previously resident); fewer than 46 (never resident) - (HMRC RDR3) |

| India | NRI general threshold | Fewer than 182 days in India in financial year - (incometaxindia.gov.in) |

| India | RNOR trigger (high-income visiting citizens) | 120–181 days + ₹15 lakh+ Indian income + 365+ days in preceding 4 years |

All figures correct as of April 2026. Tax law changes - always confirm thresholds via the cited official sources for the relevant year.

Who this guide is for: US citizens in the UK, India, or UAE; UK long-term residents with US or India financial ties; Indian-origin professionals with multi-country income; digital nomads with worldwide income and global assets; and anyone managing finances across two or more of Settel's key corridors.

The Three-Country Problem for Expats in 2026

The Three-Country Problem is what happens when an expat lives in one country, earns income in a second, and holds assets in a third - with overlapping tax rules, competing residency tests, and compliance deadlines that do not align.

It is not a niche situation. It is the default experience for globally mobile professionals in 2026.

Two people. Three countries. Neither knows what they owe.

Vikram is a US citizen, four years in Dubai, with a rental flat in Battersea and Indian equity mutual funds worth roughly £180,000. He has not filed a US return in three years, has not declared his UK rental income to HMRC, and has not reported his Indian investments to the IRS. His reasoning: he lives in the UAE, which has no income tax, so none of it applies to him.

He is wrong on all three counts.

His UK rental income is taxable in the UK regardless of where he lives. The UK has primary taxing rights on UK-sourced property income under both domestic law and international treaty law. Under the Non-Resident Landlord Scheme, his letting agent should be withholding 20% basic-rate income tax at source unless he has registered for gross payment approval with HMRC. (HMRC NRLS guidance, gov.uk) His Indian mutual fund gains are taxable in India: long-term gains on equity funds held over 12 months, where gains exceed ₹1.25 lakh, are taxed at 12.5% (post Budget 2024). And as a US citizen, he must report all of it to the IRS - worldwide income is taxable regardless of residency - and file an FBAR for every year his combined foreign account balances exceeded $10,000.

Three years of missed FBARs. Willful penalties can reach 50% of account balances per violation, per year. The UAE's zero-income-tax environment is real. It just does not cancel obligations in countries where Vikram holds assets, earns income, or holds citizenship.

Priya is an Indian-origin professional, 12 years in the UK, visiting India for 130 days in FY 2025-26 for family and work. She has ₹22 lakh in Indian-source income. She assumes she is an NRI and taxed only on Indian income in India, as usual.

The 120-day modified rule may change that. Under India's Income Tax Act, an Indian citizen or person of Indian origin with Indian-source income above ₹15 lakh who spends 120 or more days in India in the financial year and has spent 365 or more days in India across the preceding four years is classified as Resident but Not Ordinarily Resident (RNOR). Both conditions must be met - 120 days alone is not sufficient. Priya needs to check her cumulative day count before assuming NRI status. (incometaxindia.gov.in)

The cost of getting it wrong is not abstract. Missed FBAR + three years of unreported UK rental income at £20,000 per year = potential HMRC liability of ~£12,000 (tax plus interest and late filing penalties) plus FBAR exposure of up to $165,353 or 50% of relevant account balances per willful violation. Getting it right costs a fraction of that.

Fifteen years in corporate banking taught me one thing that explains most of what I see now. Banks and financial institutions are structured by jurisdiction - the UK desk, the US desk, the India desk - and so is the advice they give. Nobody at any of those desks has a bad intention. They just do not see the other two desks. So a client with a UK mortgage, a US brokerage account, and an Indian mutual fund portfolio gets three sets of advice that are each technically correct and collectively incomplete. The multi-country mistake is not usually ignorance. It is the gap between departments that nobody is paid to bridge.

Expat Asset Protection Checklist

| Action | Why it matters |

|---|---|

| Establish residency status in every country where you have ties | Determines which country taxes which income |

| Map every asset, account, and entity by jurisdiction | Identifies undisclosed structures and reporting gaps |

| File FBAR if foreign accounts exceeded $10,000 at any point | Willful penalties reach 50% of account balance per violation |

| Apply the correct DTAA to each income stream | Prevents double taxation; credits must be claimed actively |

| Verify IHT exposure if UK-resident for 10+ of last 20 years | April 2025 rules pull worldwide assets into UK IHT scope |

| Check India day count before assuming NRI status | 120-day + ₹15 lakh rule creates RNOR, not NRI classification |

| Review legal structures for unreported entities | PFIC, CFC, and trust reporting obligations are separate from income tax |

| Build a compliance calendar with single owner per obligation | Missed deadlines can unravel years of careful planning |

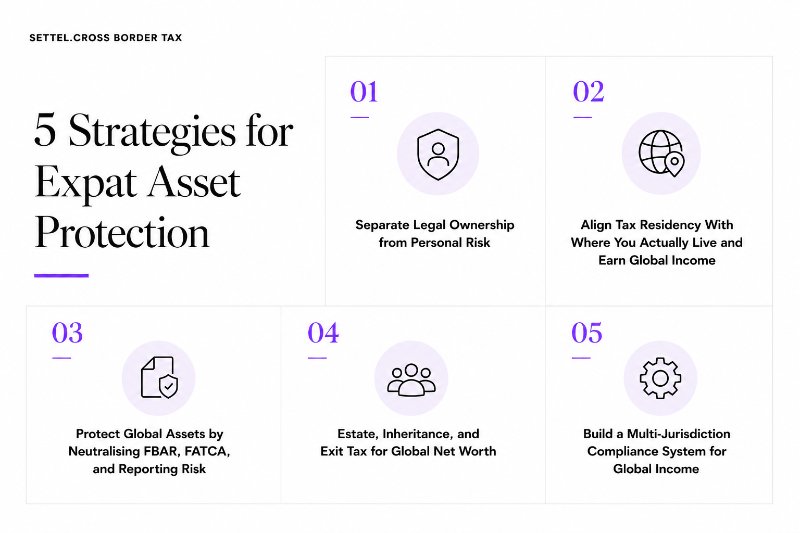

Strategy 1 - Separate Legal Ownership from Personal Risk

The key point: Trusts, LLCs, and offshore companies create legal distance between you and your assets. That distance protects against creditors, divorce claims, and litigation. The risk is not the structure itself - it is a structure that is undisclosed, mismatched with your tax position, or simply in the wrong jurisdiction for your corridor.

What is an expat asset protection trust?

A discretionary trust separates legal ownership from beneficial enjoyment. You transfer assets to a trustee who manages them for named beneficiaries. Offshore trusts in jurisdictions such as Cook Islands or Nevis require creditors to prove fraudulent intent under local law before they can touch the assets - a substantially higher evidential bar than in most common law jurisdictions.

For UK long-term residents, the April 2025 IHT reforms are directly relevant. From 6 April 2025, if the settlor is UK tax resident for 10 of the last 20 tax years, worldwide assets in a trust they have settled may be within scope of UK IHT at 40% above the nil-rate band of £325,000. Trust structures created or funded before reaching long-term resident status require review under the new rules. (HMRC IHT Manual IHTM47020)

When does a holding LLC or SPV work for expats?

US-based LLCs separate personal assets from operating and real estate risk with pass-through taxation. A foreign LLC or special purpose vehicle holding international assets is legal - but triggers reporting requirements that most holders do not know exist. Form 5471 applies to US persons owning controlled foreign corporations. Form 8865 applies to foreign partnerships. Missing these is a separate compliance failure from missing income tax returns.

When does an offshore company increase my expat tax risk?

More often than most expats expect. Three specific situations where offshore structures add risk:

PFIC exposure for US persons holding Indian mutual funds. Indian equity mutual funds are typically classified as Passive Foreign Investment Companies (PFICs) under IRC §1291. The default PFIC tax regime imposes interest charges on deferred gains at the highest ordinary income rate, applied retroactively to all years of holding - a result that is often more expensive than simply paying tax each year. QEF or mark-to-market elections are available but require annual Form 8621 filings. Holding Indian mutual funds as a US person without addressing PFIC classification is a widely misunderstood, high-consequence exposure for the US–India corridor. Specialist advice is essential before investing, not after.

UK IHT exposure under the new long-term resident rules. BVI or Cayman companies held by UK long-term residents no longer reliably shelter assets from UK IHT under the April 2025 residence-based regime.

CRS and FATCA reporting make offshore accounts visible. Over 110 countries share US account holder data with the IRS under FATCA. Most G20 jurisdictions exchange data with each other under the Common Reporting Standard. The assumption that offshore structures provide privacy from tax authorities is, in most corridors, incorrect.

Mini case study - UK property: direct ownership vs BVI company

Vikram holds his Battersea flat directly. He is subject to UK income tax on rental income (20% withheld at source under the NRLS), UK capital gains tax on disposal (28% on residential property for higher-rate non-residents), and US income tax on both - with a foreign tax credit offsetting UK tax paid.

Had he held the property through a BVI company, he would face UK Annual Tax on Enveloped Dwellings (ATED) for properties above £500,000, a 15% SDLT surcharge on acquisition, and no reduction in the CGT liability on disposal since the April 2015 extension of CGT to non-resident companies owning UK residential property. Direct ownership is more tax-efficient for UK residential property held by a non-resident individual. The BVI company adds reporting complexity without reducing the bill.

What to do: Map every entity you own or control, in every jurisdiction. Identify what is disclosed and what is not. The protection only works if the structure is visible to the right authorities.

Best for: High-net-worth individuals with business or real estate risk across multiple jurisdictions; anyone facing creditor or litigation exposure in a common law country; people planning succession across borders.

Strategy 2 - Align Tax Residency With Where You Actually Live and Earn Global Income

The key point: Tax residency is not an opinion - each jurisdiction applies a statutory test. Getting it wrong does not reduce your global tax burden; it means you pay the wrong amount to the wrong authority and miss treaty benefits you were entitled to.

How do expats determine tax residency across multiple countries?

Each country uses its own test. They do not align.

US citizens and green card holders: residency is irrelevant for income tax purposes. The US uses citizenship-based taxation - worldwide income is taxable regardless of where you live or how long you have been abroad. The FEIE ($132,900 for 2026) reduces federal income tax on foreign employment income for those meeting the Physical Presence Test (330+ days abroad in any 12-month period) or Bona Fide Residence Test. It does not shelter rental income, investment income, or capital gains.

UK - Statutory Residence Test (SRT): the SRT applies in strict order. (HMRC RDR3)

Automatic overseas tests - you are automatically non-resident if:

- Fewer than 16 UK days in the tax year (if previously UK resident in any of the prior 3 years)

- Fewer than 46 UK days (if not previously UK resident in any of the prior 3 years)

- Working full-time overseas: fewer than 91 UK days, no more than 30 UK workdays in the year

These are fewer than thresholds - 15 days or fewer, 45 days or fewer. They are not inclusive caps.

Automatic UK test - 183 or more UK days means automatic UK residence. That is a residence trigger, not a non-residence safe harbour.

Sufficient ties test - between those extremes, UK ties determine your status:

| UK days in tax year (previously resident) | Ties needed to be UK resident |

|---|---|

| Fewer than 16 | Automatic non-resident |

| 16–45 | 4 ties |

| 46–90 | 3 ties |

| 91–120 | 2 ties |

| 121–182 | 1 tie |

| 183+ | Automatic resident |

UK ties include: a UK home, a UK-resident spouse or minor child, substantive UK work, and prior UK residency (90+ UK days in either of the two preceding years). The SRT is highly fact-specific. RDR3 contains exceptions for transiting days and exceptional circumstances. No simplified summary replaces a full SRT analysis.

India - NRI and RNOR thresholds (FY 2025-26):

- 182+ days in India → resident (ROR or RNOR depending on prior year tests)

- 60+ days in current year + 365+ days in preceding four years → also resident (with exceptions for Indian citizens leaving for employment)

- 120–181 days + ₹15 lakh+ Indian-source income + 365+ days in India in preceding four years → RNOR (taxed on Indian income only)

- 120 days alone does not create RNOR; both conditions must be met

Note: The Income Tax Bill 2025, effective 1 April 2026, carries these rules forward with modifications. Confirm via current CBDT circulars for the relevant financial year.

UAE: no personal income tax. Does not override obligations in citizenship or prior residence countries.

What does multi-country tax exposure look like for expats in practice?

Example A - US/UK dual exposure (James, US citizen, 11 years UK tax resident, 2026)

| Income | UK treatment | US treatment | Net position |

|---|---|---|---|

| $300,000 salary from US employer | Not UK-taxable if duties performed outside UK | Taxable; FEIE ($132,900) offsets first portion | US tax on ~$167,100 after FEIE |

| £20,000 UK rental income | UK taxable at income tax rates; HMRC has primary rights | Must report to IRS; foreign tax credit offsets UK tax paid | Pays UK rate; claims FTC on US return - not taxed twice |

James does not pay tax twice on the rental income - the foreign tax credit neutralises the overlap. He does pay US tax on salary above the FEIE threshold. Neither obligation disappears because he lives in the UK.

Example B - India RNOR vs full resident (Priya, 130 India days, ₹22 lakh Indian income, FY 2025-26)

Priya has spent 400 days in India across the preceding four financial years. She meets all three conditions for RNOR: 120+ days in current year, ₹15 lakh+ Indian income, 365+ days in preceding four years. Result: Indian income taxable in India; UK employment income and UK assets are not taxable in India.

Had she stayed 182+ days, she would be a full Resident and Ordinarily Resident - UK salary included in Indian taxable income. The difference between 130 and 182 days is material.

Settel's day-count tracker surfaces this before the threshold is crossed, not after.

What to do: Establish your residency status in every country at the start of each tax year. Apply the relevant DTAA to each income stream. Claim foreign tax credits proactively - no authority offers them automatically.

Best for: Anyone splitting time between countries, dual citizens, recent movers, and anyone with income flowing across two or more of Settel's key corridors.

Strategy 3 - Protect Global Assets by Neutralising FBAR, FATCA, and Reporting Risk

The key point: FBAR penalties are tied to account balances, not to tax owed. The exposure can exceed the value of the account itself. Over 110 countries share US account holder data with the IRS through FATCA. Assuming invisibility is not a strategy.

What are the 2026 FBAR and FATCA thresholds for US expats?

FBAR (FinCEN Form 114) - Bank Secrecy Act, 31 U.S.C. §5321:

File if aggregate foreign financial account balances exceed $10,000 at any point in the calendar year. Deadline: April 15, with an automatic extension to October 15. (IRS FBAR guidance)

FATCA (Form 8938) - Internal Revenue Code:

File with your federal tax return if foreign financial assets exceed $200,000 at year-end (or $300,000 at any point) for single filers living abroad.

What happens to expats who miss FBAR filings for several years?

| Scenario | Violation type | Approximate penalty exposure | Remediation path |

|---|---|---|---|

| $50,000 offshore, 3 years non-filing, income properly reported, no IRS contact | Non-willful | Up to ~$16,536 per year (per FBAR form, not per account - Bittner v. United States, SCOTUS 2023); often $0 with voluntary filing | Delinquent FBAR Submission Procedures (DFSP) - $0 penalty if income reported and IRS not yet in contact |

| $1,000,000 offshore, apparent willful non-disclosure, IRS investigation underway | Willful | Up to $165,353 or 50% of account balance per violation, per year - can exceed total account value across multiple years | Voluntary Disclosure Programme - outcome depends on facts and legal representation |

FBAR and FATCA are separate systems with separate statutory bases. Both can apply simultaneously to the same account. Penalty amounts are adjusted for inflation and shaped by evolving case law - always verify current figures via IRS and FinCEN guidance before relying on any specific dollar amount.

FATCA penalty structure:

| Violation | Penalty |

|---|---|

| Failure to file Form 8938 | $10,000 fixed |

| Continued failure after IRS notice | Up to $50,000 additional |

| Underpayment attributable to undisclosed assets | 40% of tax underpayment |

What to do: Audit every foreign account, investment, and financial interest. If you are behind on FBARs and your income was properly reported, Streamlined Foreign Offshore Procedures or DFSP are available before the IRS contacts you. The window closes the moment contact is made.

Best for: All US citizens and green card holders with any financial account outside the US, regardless of where they live.

Strategy 4 - Estate, Inheritance, and Exit Tax for Global Net Worth

The key point: US citizens face estate tax on worldwide assets above $15,000,000 in 2026. UK long-term residents - anyone resident for 10 of the last 20 UK tax years - face IHT at 40% on worldwide assets above £325,000 from April 2025. The two exposures can overlap. Neither disappears because assets are held in a third country.

How do US estate tax and UK inheritance tax interact for expats?

UK IHT (from April 2025):

NRB: £325,000 per individual; RNRB: £175,000 additional when main home passes to direct descendants (tapers above £2m estate). Combined: up to £500,000 per individual; up to £1m per couple. (HMRC, gov.uk)

Rate: 40% above allowances.

Long-term resident trigger: 10 of last 20 UK tax years. Worldwide assets in scope. IHT tail after leaving UK: 3-10 years depending on total years of UK residence.

US federal estate tax:

Exemption 2026: $15,000,000 per individual; $30,000,000 per couple with portability. (IRS)

Rate: 40% above exemption. Permanent under One Big Beautiful Bill Act (P.L. 119-21, July 2025); inflation-indexed from 2027. Future legislation could alter it - confirm for the year of any transfer or death.

The overlap - a worked illustration

A US citizen, 12 years UK tax resident, with a worldwide estate of approximately $20,000,000: UK home (£2.5m), US investment portfolio ($5m), Dubai property (£1.5m), Indian equity mutual funds (₹1.5 crore / ~£1.4m).

| Jurisdiction | Assets in scope | Threshold | Approximate gross exposure (no planning) |

|---|---|---|---|

| UK IHT | Worldwide assets (12 years UK resident = long-term resident) | £325,000 NRB + £175,000 RNRB on UK home to direct descendants | 40% on ~£6.5m above allowances ≈ £2.6m |

| US estate tax | Worldwide assets (US citizen) | $15,000,000 | 40% on ~$5m above exemption ≈ $2m |

| Overlap | Same assets taxed in both jurisdictions | - | Without treaty relief, exposure on overlapping assets is additive |

The US–UK Estate and Gift Tax Treaty coordinates taxing rights and provides foreign tax credits so the same assets are not taxed at full rate in both countries simultaneously. Primary taxing rights are assigned based on treaty domicile; foreign tax credits reduce the second country's charge by tax paid to the first. The treaty does not eliminate double taxation - it reduces it. Exact outcomes depend on domicile determination, asset location, treaty elections, and timing, and require specialist cross-border estate planning advice. (IRS, US-UK treaty documents)

When does exit tax planning become relevant for expats?

| Factor | Relevance |

|---|---|

| Net worth ≥ $2,000,000 | Covered expatriate test triggered |

| Average annual US tax ≥ $206,000 in prior 5 years | Second covered expatriate test |

| Non-compliant with US tax certification | Third covered expatriate test - triggered regardless of wealth |

| Significant non-US assets (Indian mutual funds, UK property, UAE real estate) | All included in the §877A deemed sale calculation |

| Deferred compensation or US pension | Different treatment - 30% withholding applies |

The 2026 exit tax exclusion is $910,000 (IRC §877A, inflation-indexed annually). This is a per-person exclusion on net unrealised gains - not on total assets. Confirm the current exclusion via the then-current Form 8854 instructions for the relevant tax year. (IRS expatriation tax)

Renunciation is irreversible. The tax consequences interact with your entire asset base across every jurisdiction. This requires specialist advice in every country where you hold assets.

What to do: If your combined estate approaches the relevant thresholds in any jurisdiction, model the multi-jurisdiction overlap before it becomes a problem. Settel's NPV Engine and Scenarios tab are built for this.

Best for: US citizens with significant non-US assets, long-term UK residents past or approaching the 10-year IHT trigger, dual citizens, and anyone managing an estate across two or more jurisdictions.

Strategy 5 - Build a Multi-Jurisdiction Compliance System for Global Income

The key point: Every other strategy in this list depends on this one. Perfect structures fail when a filing deadline is missed. A system is what keeps them intact.

How can expats legally reduce global tax on multi-country income?

The answer is not clever structures - it is systematic compliance that preserves the structures you already have. Most expat tax leakage comes not from bad planning but from good planning that breaks down in execution: the FBAR that nobody filed, the treaty credit that was never claimed, the residency status that was not updated after a move.

The four-step compliance process:

Step 1 - Inventory. List every jurisdiction where you hold assets, earn income, or claim residency. List every entity, account, investment, and property. Update it annually.

Step 2 - Map obligations and deadlines.

| Jurisdiction | Key obligation | Threshold | Deadline |

|---|---|---|---|

| US | FBAR (FinCEN 114) | $10,000 aggregate foreign accounts at any point | April 15 (Oct 15 automatic extension) |

| US | Form 8938 (FATCA) | $200,000 abroad at year-end / $300,000 at any point (single, overseas) | With federal tax return |

| US | Federal income tax (Form 1040) | All worldwide income - no threshold for citizens | April 15; June 15 if residing abroad; Oct 15 extension available |

| UK | Self Assessment | Any UK-taxable income | 31 January |

| India | ITR filing | Income above basic exemption limit (₹2.5 lakh old regime / ₹3 lakh new regime for NRIs) | 31 July of assessment year |

| UAE | Corporate tax registration | Businesses earning above AED 375,000 | Varies by financial year-end |

Step 3 - Assign one owner per obligation. One person or one system is responsible for each filing. Not three accountants in three countries who do not communicate.

Step 4 - Review annually. Tax law changes. Residency changes. Asset composition changes. A compliance system is a living document, not a one-time exercise.

What does missing three years of FBARs actually cost?

| Scenario | Outcome |

|---|---|

| $200,000 offshore, income reported, voluntary disclosure under DFSP before IRS contact | $0 penalty - but requires filing 3 years of FBARs, reasonable cause statement, and professional time |

| Same - but IRS contact received before disclosure | Up to ~$16,536 per year; potentially reduced for reasonable cause |

| Same - but wilful | Up to 50% of $200,000 per violation per year = up to $300,000 across 3 years, exceeding total account balance |

The cost of structured compliance (a tracking platform and a tax professional) is a fraction of the cost of remediation. And remediation only works before the IRS contacts you.

Best for: Anyone with obligations in two or more jurisdictions. This applies to every Settel user.

Settel tracks your day counts, asset values, and compliance deadlines across jurisdictions in one place - so when you sit down with your advisers, you are working from a single accurate picture instead of three spreadsheets and a best guess. I built it for the situation this guide describes. [Start the current Settel trial → app.settel.io]

Frequently Asked Questions for Expats and Digital Nomads

Do digital nomads pay tax on worldwide income in their home country?

It depends on the home country's tax system. The US and Eritrea are the only countries that tax citizens on worldwide income regardless of where they live - a US citizen in Bali with no US income still files a US return. Most other countries use a residence-based system: if you spend 183 or more days in a year in a country (or establish sufficient ties there), that country taxes your worldwide income. A UK citizen who cleanly establishes non-residence under the SRT stops being taxed on worldwide income in the UK. A digital nomad who does not clearly establish tax residency anywhere may inadvertently retain it in their home country through ties such as a bank account, a property, or family - and face a worldwide tax liability they did not expect.

How can expats legally reduce global tax on multi-country income?

The main tools are: the Foreign Earned Income Exclusion (US, $132,900 for 2026 on qualifying employment income abroad); foreign tax credits, which offset tax paid in one country against liability in another on the same income; Double Taxation Agreements, which assign primary taxing rights to prevent the same income being taxed in full in two places; and residency planning, which ensures you are resident where the rules are most favourable for your income type. None of these work if you do not file the correct forms. The FEIE requires Form 2555. Foreign tax credits require Form 1116. Treaty positions require Form 8833 in some cases. The legal reduction of global tax is a filing exercise, not an avoidance strategy.

What happens if expats miss FBAR filings for several years?

If your income was properly reported and you act before the IRS contacts you, the Delinquent FBAR Submission Procedures (DFSP) allow voluntary filing with typically $0 penalty. If the IRS contacts you first, non-willful penalties can reach ~$16,536 per FBAR form (not per account, following Bittner v. United States). If the violation is deemed willful, penalties reach the greater of ~$165,353 or 50% of the account balance, per violation, per year - an exposure that can exceed the total account value across multiple years. Criminal prosecution is possible for serious willful non-disclosure. The gap between "non-willful" and "willful" is determined by the IRS based on facts - checking "No" on Schedule B when you knew you had foreign accounts is evidence of willfulness. Act before contact; the window closes the moment the IRS reaches out.

When does an expat become Resident but Not Ordinarily Resident (RNOR) in India?

RNOR status under India's Income Tax Act arises in three situations: (1) you were a non-resident in 9 of the 10 preceding financial years; (2) you spent 729 or fewer days in India in the 7 preceding financial years; or (3) you are an Indian citizen or person of Indian origin who visits India for 120 to 181 days in the financial year, has Indian-source income exceeding ₹15 lakh, and has spent 365 or more days in India across the preceding four financial years. All three conditions in scenario (3) must be met - 120 days alone is not sufficient. RNOR status means you are taxed on Indian income only, not on worldwide income. It is relevant primarily for returning NRIs and high-income visiting professionals, and the distinction between RNOR and full resident (ROR) can be significant where the individual has substantial foreign income.

If I'm under the US estate tax exemption, do I still need a cross-border estate plan?

Yes. The $15,000,000 US estate tax exemption (2026) removes most expats from federal estate tax exposure - but it does not address UK inheritance tax for long-term residents (40% above £325,000 on worldwide assets), Indian succession obligations for assets held in India, or the non-citizen spouse limitation (only a $175,000 marital deduction applies when the surviving spouse is not a US citizen, versus an unlimited deduction for US citizen spouses). A US citizen in the UK with a £2m estate and a non-citizen spouse may face significant UK IHT with zero US estate tax exposure. Cross-border estate planning is about more than the federal threshold.

Can I safely hold Indian mutual funds as a US person?

This is one of the most widely misunderstood exposures for US citizens invested in Indian markets. Indian equity mutual funds are typically classified as Passive Foreign Investment Companies (PFICs) under IRC §1291. The default PFIC regime imposes interest charges on deferred gains at the highest ordinary income rate, applied retroactively to all years of holding - often worse than simply paying tax each year. Elections are available (QEF or mark-to-market) but require annual Form 8621 filings and ongoing compliance. Holding Indian mutual funds as a US person without addressing PFIC classification is a material unmanaged risk. Get specialist US tax advice before investing, not after.

When does it make sense to consider renouncing US citizenship for asset protection?

Rarely, and only after exhausting every other option. Renunciation is irreversible. It triggers the IRC §877A exit tax on worldwide assets for "covered expatriates" (net worth ≥$2m, average annual US tax ≥$206,000 over the prior 5 years, or non-compliance with tax certification). The 2026 gain exclusion is $910,000 - gain above that is subject to capital gains tax on a deemed sale of all worldwide assets the day before expatriation. Deferred compensation and US pensions are treated differently, with 30% withholding applying. Five years of certified US tax compliance is required for a clean renunciation. For most expats below $2m net worth, exit tax is zero - but the compliance cost of getting there cleanly is not. Renunciation makes sense for people with very large non-US estates, no meaningful ongoing US connection, and a clear alternative citizenship plan. It is not a quick solution and never an asset protection shortcut.

How does Settel work alongside my tax advisers in each country?

Settel provides the data layer: asset values across currencies, day counts by jurisdiction, compliance deadline calendar, and scenario modelling using current 2026 thresholds. Your advisers provide the judgement layer: treaty interpretation, residency determinations, and filing strategy. Most expats have separate advisers in each country who rarely share information. Settel creates a single source of truth that you bring to every adviser conversation, so you are not reconstructing your position from scratch each time. Settel AI (coming soon) will surface relevant treaty provisions and flag residency changes as they happen, making those conversations more targeted and less expensive.

Protect What You Have Built Across Borders

Settel is built for people who are done reconstructing their financial picture from three different spreadsheets.

The Smart Tax Engine calculates your obligations across jurisdictions. The day-count tracker monitors your residency position in real time. Compliance deadline reminders mean you will not miss an FBAR or a self-assessment filing because it slipped between two accountants in two countries.

Start tracking your global income and assets →

Related corridors and guides: How global tax treaties work for expats → · UK expat tax guide → · US expat taxes → · India NRI taxes → · UAE expat taxes →

Informational only - not financial advice. Settel is a tracking and calculation tool. Always consult a qualified tax professional for advice specific to your situation.