What is tax treaty relief? A 2026 guide for expats

Most expats assume they're stuck paying taxes in both their home and host countries. That's rarely true. Tax treaty relief exists precisely to prevent this double taxation nightmare, yet countless globally mobile professionals miss out on these benefits simply because they don't understand how treaties work or how to claim them. This guide breaks down what tax treaty relief is, how it operates across the US, UK, India, and UAE, and why mastering it in 2026 can save you thousands while keeping you compliant.

Table of Contents

- What Is Tax Treaty Relief And Why Does It Matter?

- How Tax Treaty Relief Works: Key Concepts And Mechanisms

- Navigating Tax Treaty Relief For US, UK, India, And UAE Expats

- Common Challenges And How To Maximize Tax Treaty Relief Benefits

- How Settel Supports Your Tax Treaty Relief Needs

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Prevents double taxation | Tax treaty relief stops you from paying tax on the same income in multiple countries |

| Requires proper documentation | You must meet residency tests and file specific forms to access treaty benefits |

| Works through three mechanisms | Relief comes via exemption, foreign tax credit, or reduced withholding rates |

| Eligibility varies by treaty | Each bilateral agreement has unique provisions based on your residency and income type |

| Missing claims costs money | Failing to claim treaty relief properly means overpaying taxes and risking penalties |

What is tax treaty relief and why does it matter?

Tax treaty relief is a mechanism that reduces or eliminates double taxation when your income could be taxed in two countries. It stems from bilateral agreements called tax treaties or Double Taxation Avoidance Agreements (DTAAs) that countries negotiate to clarify which nation has primary taxing rights over specific income types.

These treaties determine whether your salary, dividends, rental income, or capital gains get taxed in your country of residence, your country of source, or both with offsetting credits. Without treaty relief, you'd face the same income being taxed twice, which quickly becomes unsustainable for anyone earning across borders.

For professionals moving between the US, UK, India, and UAE, treaty relief matters enormously. These four countries maintain extensive treaty networks precisely because so many people earn, invest, and hold assets across these jurisdictions. The UAE's zero personal income tax creates unique dynamics, while the US taxes worldwide income regardless of where you live, making treaty provisions critical for avoiding crushing tax bills.

Key features and benefits include:

- Allocates taxing rights between countries based on income type and residency status

- Provides legal certainty about where you owe tax and how much

- Reduces withholding taxes on cross-border payments like dividends and royalties

- Offers foreign tax credits to offset taxes paid in one country against obligations in another

- Protects against discriminatory taxation of foreign nationals

- Establishes dispute resolution procedures when countries disagree on treaty interpretation

Understanding these provisions transforms tax planning from reactive scrambling to proactive optimization. You stop overpaying and start structuring your income and investments with clarity.

How tax treaty relief works: key concepts and mechanisms

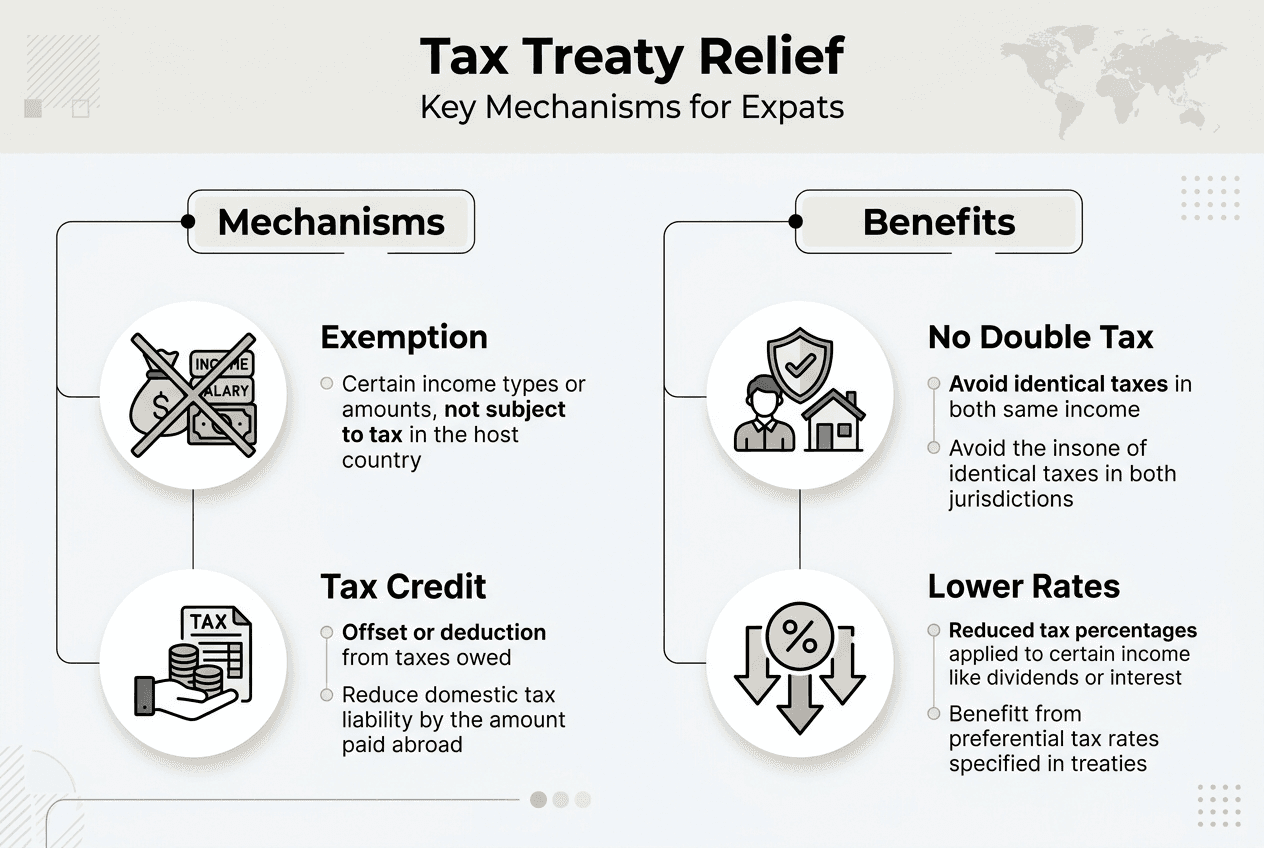

Treaty relief operates through three main mechanisms: exemption, foreign tax credit, and reduced withholding rates. Each serves different situations, and tax treaties typically provide methods like exemption, credit, and reduced withholding tax rates depending on the income type and treaty provisions.

Exemption means one country agrees not to tax specific income at all, eliminating double taxation at the source. If you're a UK resident earning employment income in India under a treaty exemption, India might not tax that salary, leaving only UK tax obligations. This is clean and simple when it applies.

Foreign tax credit allows you to offset taxes paid in one country against your tax bill in another. If you paid $5,000 in US tax on investment income and owe $7,000 in UK tax on the same income, you credit the $5,000 against your UK bill, paying only the $2,000 difference. The credit prevents paying full tax twice, though you still pay up to the higher rate.

Reduced withholding rates lower the tax taken at source on cross-border payments. Without a treaty, a country might withhold 30% tax on dividends paid to foreign residents. Treaties often reduce this to 15% or 10%, letting you keep more of your income upfront.

| Mechanism | How it works | Best for | Limitation |

|---|---|---|---|

| Exemption | One country doesn't tax the income | Employment income, pensions | Must qualify under treaty provisions |

| Foreign tax credit | Offset tax paid abroad against domestic tax | Investment income, business profits | Limited to the lower of taxes paid or owed |

| Reduced withholding | Lower tax rate at source | Dividends, royalties, interest | Still requires claiming and documentation |

Claiming tax treaty relief follows a clear process:

- Determine your tax residency status in each relevant country using their domestic rules

- Identify which treaty applies based on the countries involved

- Review the specific treaty article covering your income type

- Obtain a certificate of tax residency from your country's tax authority

- Submit the required forms to claim treaty benefits in the source country

- Report the income correctly on your tax returns in both jurisdictions

- Keep detailed records of all income, taxes paid, and relief claimed

Pro Tip: Residency certificates expire and take weeks to obtain. Request yours at least 60 days before you need to claim treaty benefits, and keep digital copies with your tax records for quick access during filing season.

Navigating tax treaty relief for US, UK, India, and UAE expats

Each of these four countries approaches treaty relief differently, creating a complex web when you earn or invest across multiple jurisdictions. The US taxes citizens and residents on worldwide income, making treaties essential for offsetting foreign taxes. The UK uses statutory residency tests and split year treatment. India distinguishes between residents, non-residents, and not ordinarily resident status. The UAE has no personal income tax but maintains treaties affecting business income and withholding.

Key treaty relationships include the US-UK treaty covering employment, pensions, and investment income with generous provisions for expats. The US-India treaty addresses software royalties and technical services, critical for tech professionals. The UK-India treaty provides relief on pensions and social security. The UAE's treaties with these countries focus primarily on business profits and withholding taxes since there's no personal income tax to relieve.

Residency criteria determine everything. The US uses the substantial presence test (183 days over three years with a weighted formula) or green card status. The UK applies the statutory residence test examining ties like family, accommodation, and work. India counts 182 days in a tax year or 60 days in the current year plus 365 in the prior four years. When you're resident in multiple countries simultaneously, treaty tie-breaker rules use factors like permanent home, center of vital interests, and habitual abode to determine your treaty residence.

Documentation requirements vary but commonly include:

- Form 8833 for US taxpayers claiming treaty positions that reduce US tax

- Certificate of Residence from HMRC for UK residents claiming treaty benefits abroad

- Form 10F in India for non-residents claiming treaty relief

- Tax Residency Certificates authenticated by relevant authorities for UAE-based professionals

- Detailed records of days present in each country supporting your residency claims

- Bank statements and payment records proving where income was earned and taxed

Common pitfalls include missing filing deadlines, which can permanently forfeit treaty benefits for that tax year. Expats often incorrectly report income by failing to distinguish between treaty-exempt and taxable amounts. Others claim relief without proper residency certificates, triggering audits and penalties. Some assume UAE residence automatically eliminates all tax, missing obligations in countries that tax based on citizenship or source.

Pro Tip: Set up a shared calendar with all relevant tax deadlines across your countries of obligation. The US deadline (April 15, extended to June 15 for expats), UK self-assessment (January 31), and India filing dates (July 31) don't align, and missing any one can trigger penalties that dwarf the tax you're trying to save.

Common challenges and how to maximize tax treaty relief benefits

The biggest challenge isn't the treaties themselves but the interaction between treaty provisions and domestic tax rules. Many expats misunderstand treaty provisions by reading articles in isolation without considering how domestic law applies first. Treaties provide relief from double taxation but don't create tax obligations that don't exist under domestic law. If your income isn't taxable under a country's domestic rules, the treaty is irrelevant.

Missing filing deadlines remains the most expensive mistake. Countries impose strict deadlines for claiming treaty benefits, and late claims often get denied entirely. Some jurisdictions allow amended returns, but others treat late treaty claims as new positions requiring disclosure and justification.

Insufficient records sink treaty claims during audits. Tax authorities want proof of residency, proof of foreign taxes paid, and documentation showing the income qualifies for treaty treatment. Without contemporaneous records, you're arguing from memory against auditors with statutory authority.

"Expats must meet residency tests and file specific forms to access treaty relief in US, UK, India, and UAE, yet documentation errors cause most claims to fail during review."

Working with tax professionals familiar with international treaties stops these problems before they start. Generalist accountants often lack cross-border expertise, while international tax specialists understand treaty nuances, tie-breaker rules, and filing procedures across jurisdictions. The cost of professional help is typically far less than the tax saved plus penalties avoided.

Top strategies for maximizing benefits:

- Review your residency status annually as your circumstances change

- Claim foreign tax credits even when you think you don't owe tax in your residence country

- Structure income timing to optimize treaty benefits across tax years

- Maintain separate records for each country showing income sources and taxes paid

- Use treaty provisions for pensions and social security, often overlooked by expats

- Consider treaty shopping risks if you're structuring through multiple jurisdictions

- Leverage reduced withholding rates by providing treaty certificates to payers upfront

- Track currency exchange rates used for foreign tax credit calculations

Pro Tip: Keep all tax-related documents for at least seven years across all jurisdictions. Different countries have different statute of limitations periods, and some extend these during audits. Digital storage with cloud backup ensures you can produce records instantly if questioned, even years later.

How Settel supports your tax treaty relief needs

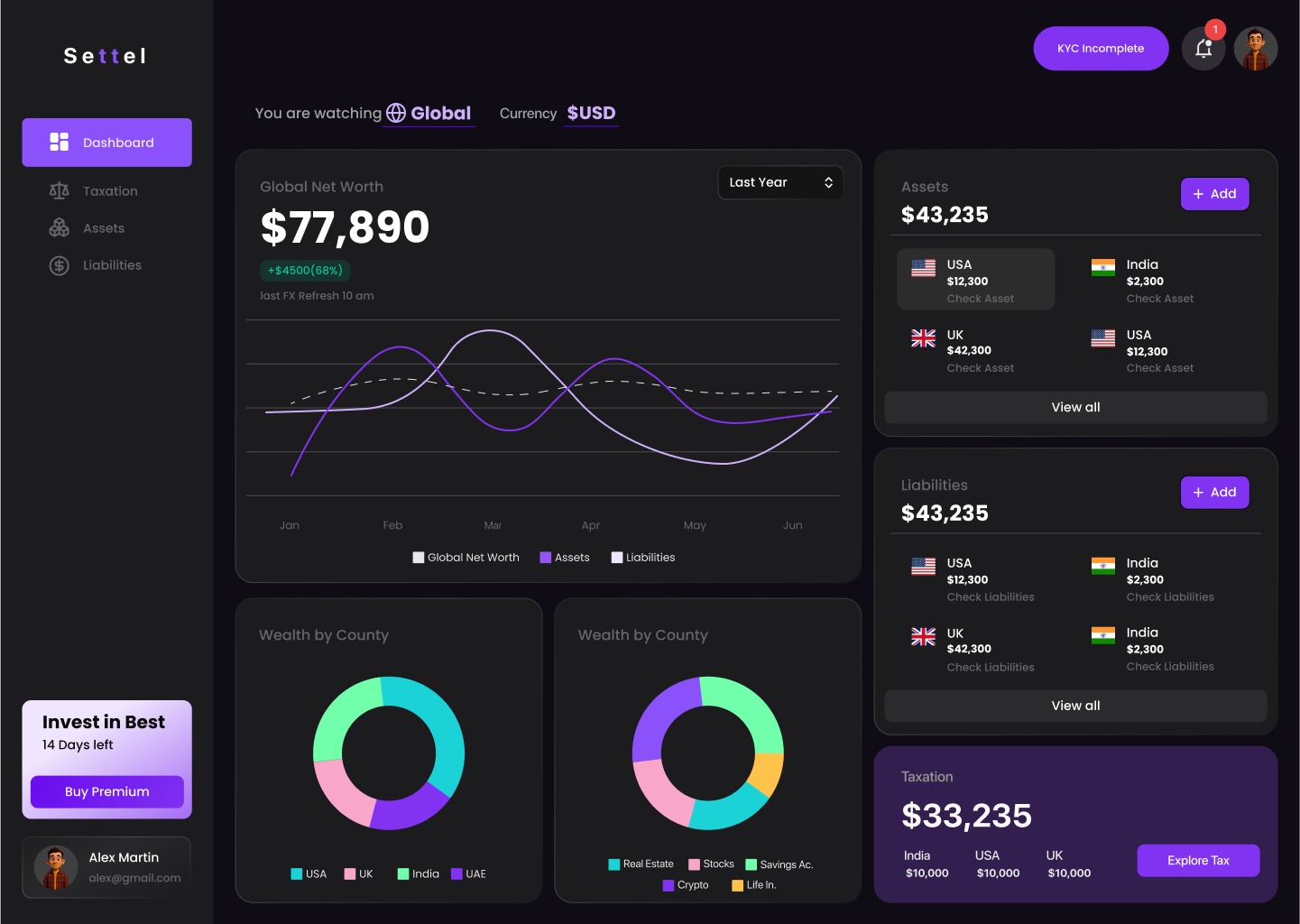

Navigating tax treaties across the US, UK, India, and UAE requires tracking residency status, modeling tax obligations under different scenarios, and ensuring you claim every benefit you're entitled to. Settel's platform was built specifically for this complexity, analyzing your residency status, income sources, and applicable treaty provisions to surface exactly what you owe in each country.

The Smart Tax Engine models Double Taxation Agreements, foreign tax credits, and tie-breaker rules automatically, showing your estimated obligations per country in real time. You're not guessing whether you qualify for treaty relief or manually calculating foreign tax credits. The platform does it, backed by validation across 88+ test cases with 100% accuracy.

Key benefits include:

- Multi-currency wealth tracking across bank accounts, investments, and property

- Automated residency analysis using your actual presence and ties in each country

- Treaty relief calculations showing exemptions, credits, and reduced rates you qualify for

- Compliance deadline reminders so you never miss a filing window

- Secure document extraction that processes your financial records and immediately deletes originals

Whether you're claiming foreign tax credits on US returns, obtaining UK residency certificates, or navigating India's treaty provisions, Settel gives you clarity before you file. Explore how the platform can simplify your global tax obligations at settel.io.

Frequently asked questions

What does tax treaty relief mean for expats?

Tax treaty relief means you can reduce or eliminate double taxation when you earn income that could be taxed in multiple countries. It works through bilateral agreements that allocate taxing rights and provide mechanisms like exemptions or credits to prevent paying full tax twice on the same income.

How do I know if I'm eligible for tax treaty relief?

Eligibility depends on your tax residency status and whether a treaty exists between the relevant countries. You must be a resident of one treaty country under its domestic law, and the income type must be covered by the treaty. Review the specific treaty articles and consult with a tax professional to confirm your eligibility.

What documents do I need to claim treaty benefits?

You typically need a certificate of tax residency from your country's tax authority, specific treaty claim forms (like Form 8833 in the US or Form 10F in India), and records proving where income was earned and taxes paid. Each country has different requirements, so check the treaty protocol and domestic filing instructions.

Can I claim tax treaty relief if I'm a digital nomad?

Yes, but it's complicated. Digital nomads must first establish tax residency somewhere, which requires meeting that country's residency tests. Without clear residency, you can't claim treaty benefits. If you're resident in multiple countries, treaty tie-breaker rules determine your treaty residence, which then governs which benefits you can claim.

What are the risks of not claiming tax treaty relief properly?

Failing to claim treaty relief means overpaying taxes, sometimes substantially. Claiming it incorrectly can trigger audits, penalties for underreporting income, and interest on unpaid taxes. Some countries treat improper treaty claims as tax evasion if they believe you intentionally misrepresented your situation. Always document your claims thoroughly and seek professional guidance when unsure.

Recommended

- 3 Types of Global Tax Treaties: 90% of Nations Use DTAAs | Settel Blog | Settel

- Global Tax Reporting: Avoid 75% Penalties in 2026 | Settel Blog | Settel

- Expat Asset Protection: 5 Strategies with 100% Compliance | Settel Blog | Settel

- Settel Expats: Wealth Management & Tax for Expats in US, UK, UAE, India