**⚠️ Important Disclaimer:** This content is for educational and informational purposes only and does not constitute financial, tax, or legal advice. Tax laws are complex and subject to change. Always consult with a qualified tax advisor or accountant regarding your specific circumstances before making any tax-related decisions.

When you're managing tax obligations across multiple countries, standard calculators often fall short. We've explored why calculators fail the Three-Country Problem - they assume a single-country life that you're no longer living.

They count days. They ignore ties. They miss treaties. And the gap between their estimates and reality can be significant.

So how do you know if the tax calculator you're using right now is giving you reliable numbers or potentially misleading estimates?

Here's the test.

Your Multi-Jurisdiction Tax Accuracy Checklist: The 3-Point Test

Before you trust any online number from a tax calculator, check these three things to see if the tool is actually built for your multi-country tax situation.

1. Check the Calendar: Tax Year Alignment Across Jurisdictions

Does the tool ask for your move date?

This sounds simple. But it's the single most revealing question about whether a calculator understands multi-jurisdiction taxation.

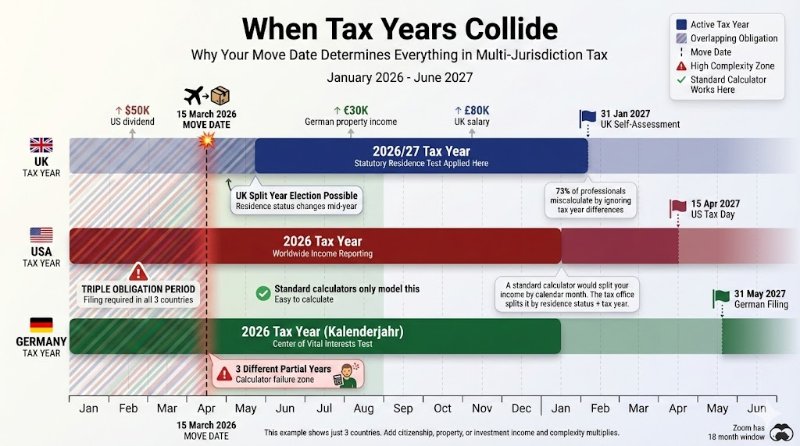

Here's why it matters: different countries have different tax years. The UK runs April to April. The US runs January to January. Australia runs July to July. If you move between countries mid-year, you don't just have two tax years to navigate. You have partial years, overlapping obligations, and split-year treatment rules that can significantly affect your tax position.

Let's say you moved from London to New York on March 15, 2026.

A calculator that only asks "What's your income?" will assume you had one tax year. In reality, you had three different partial years to navigate:

- UK tax year 2025/26 (April 2025 - March 2026): You were resident for 11.5 months

- US tax year 2026 (January - December): You became resident in March

- UK tax year 2026/27 (April 2026 onward): Your residency status may have changed

Each of these has different rules, different allowances, and different rates. If your calculator doesn't ask when you moved, it may be providing estimates that don't reflect the complexity of your actual tax position.

🚩Red flag: If the calculator assumes calendar year equals tax year, this is a fundamental limitation. This is critical to accurate multi-jurisdiction tax calculations, and something most generic tools don't address.

2. The "Tie" Test: Beyond Simple Day Counting in Multi-Country Residency

Does it ask about your family, home, or work ties?

This is where calculators reveal whether they understand modern multi-jurisdiction tax residency tests or whether they're using outdated models.

The old model was simple: 183 days in a country = resident. Fewer than 183 days = non-resident. Done.

That model is no longer sufficient.

In 2026, tax residency tests have evolved. The UK has the Statutory Residence Test. Germany uses "Center of Vital Interests." The US has the Substantial Presence Test with exceptions for closer connections. Nearly every developed country now looks beyond physical presence to understand where your life actually centers.

If your calculator only asks "How many days were you in the UK?", it may be missing the entire framework that HMRC actually uses to determine your residency status.

Here's what actually matters in the UK's Statutory Residence Test:

Family Tie: Is your spouse or minor children in the UK for more than 91 days?

Accommodation Tie: Do you have a UK home available for more than 91 days where you spend at least one night?

Work Tie: Do you work in the UK for 40 or more days (where 3+ hours counts as a work day)?

90-Day Tie: Were you in the UK for 90+ days in either of the past two tax years?

Country Tie: Did you spend more days in the UK than any other single country?

These ties can matter more than your day count. You might spend only 120 days in the UK and still be considered a tax resident if you have sufficient ties. Conversely, you could spend 150 days there and remain non-resident if you have no ties.

Consider the professional who moved from London to Switzerland. They kept their London flat available while searching for a home in Zurich. Because they had a home in the UK for more than 91 days and spent at least 30 days there, they met the "Only Home" test under the SRT - even though their day count suggested non-residency.

🚩 Red flag: If the calculator only counts days, it may be missing the core of modern multi-jurisdiction tax residency tests. These ties often significantly affect your cross-border tax obligations.

3. Verify the DTA: Double Taxation Agreement Coverage

Does it mention the Double Taxation Agreement (DTA) between your countries?

This is the test many calculators fail. And it's where significant opportunities can be missed.

Here's a common scenario: You live in the UK. You have US stock investments that pay dividends. When those dividends are paid, the US automatically withholds 30% tax at source. A basic calculator sees that withholding and treats it as final tax.

What many calculators don't account for: there's a DTA between the US and UK that may reduce the withholding rate to 15% for UK residents who properly claim treaty benefits. This requires understanding which treaty provisions apply and how to claim them.

DTAs are complex. They vary by country pair. They have different rules for different income types (employment income, dividends, interest, pensions). They require active claims through proper tax filing, not automatic application. And they can significantly affect your tax position when you're dealing with the Three-Country Problem.

Close to 3 in 5 professionals with cross-border investment income may be missing opportunities because they're unaware of how DTAs apply to their specific situations. Many accept default withholding rates when they could potentially claim treaty relief - if they knew to ask about it.

If your calculator doesn't factor in treaty provisions, you may be looking at estimates based on default withholding rates rather than treaty rates. Tax treaty benefits can make a meaningful difference in your multi-jurisdiction tax planning, but only if your calculator actually recognizes and accounts for them.

🚩 Red flag: No mention of DTAs means the calculator may be using worst-case default rates, not the treaty rates that might apply to your situation.

What the Test Reveals

Run your current calculator through these three questions:

- Does it ask when you moved?

- Does it ask about your family, home, and work ties?

- Does it account for Double Taxation Agreements?

If the answer to any of these is "no," the number you're looking at may not reflect the full complexity of your multi-jurisdiction tax situation.

The Bigger Picture

The goal isn't to make you skeptical about every tax calculation. The goal is to help you distinguish between tools that understand multi-country complexity and tools that assume a simpler scenario.

If your life spans multiple countries, you deserve tools and information that reflect that reality. Not tools that force you into a single-country framework and hope for the best.

We're building Settel as a financial tracking and planning platform for professionals facing the Three-Country Problem: earning in one currency, living in another, with obligations in a third. Similar to how Finary tracks your wealth across borders, we focus on helping you understand your cross-border tax position.

We don't provide tax advice. We provide information and planning scenarios. We show you how your multi-country tax residency status might shift based on your travel and your ties. We help you understand which Double Taxation Treaties could apply to your situation. We account for different tax years, not just calendar years.

We give you the information and scenario modeling you need to have more informed conversations with your partner, family and qualified tax advisor - someone who can provide the personalized advice your situation requires.

The gap between "what a calculator shows" and "what your tax office determines" shouldn't come as a surprise.

*Stop trying to fit your global life into a local box.*

Join the Settel waitlist today to get clarity on your multi-jurisdiction tax position through better information and planning tools - then work with your tax advisor to make the right decisions for your specific situation.

FAQ: Common Multi-Jurisdiction Tax Questions

What is the Three-Country Problem in taxation?

The Three-Country Problem occurs when you earn income in one country, live in a second country, and have tax obligations (through citizenship, property, or prior residency) in a third country. This creates complex multi-jurisdiction tax scenarios where you must navigate three different tax systems, potentially conflicting tax years, multiple currencies, and various Double Taxation Agreements. Standard tax calculators typically aren't built to handle this level of cross-border complexity.

How do I know if I'm a tax resident in multiple countries?

You can be considered a tax resident in multiple countries simultaneously if you meet each country's residency test. The UK uses the Statutory Residence Test (based on days and ties), Germany uses Center of Vital Interests (based on where your personal and economic life centers), and the US uses Substantial Presence (based on a three-year formula). If you meet the criteria in two or more countries, you're a dual resident, and tax treaties may provide tie-breaker rules to determine which country has primary taxing rights. Professional tax advice is essential for determining your status.

What's the difference between tax withholding and final tax?

Tax withholding is what's automatically deducted when you receive income (like the 30% withheld on US dividends paid to non-residents). Final tax is what you actually owe after considering tax treaties, deductions, and credits. Many people mistakenly treat withholding as final tax. If a Double Taxation Agreement exists, you may be able to claim a reduced rate (like 15% instead of 30%) or credit the withheld amount against your home country tax liability. However, these benefits typically require active claims through proper tax filing.

Can I avoid double taxation in multi-jurisdiction situations?

Double Taxation Agreements (DTAs) between countries are designed to help prevent or mitigate double taxation. These treaties determine which country has primary taxing rights and often provide mechanisms for tax credits or reduced rates. However, you typically must actively claim these benefits through proper tax filing in each jurisdiction—they're not automatically applied. Given the complexity of DTAs and how they interact with domestic tax laws, professional tax advice is strongly recommended to ensure you're properly claiming available relief.

**Disclaimer:** The information provided in this article is for general educational purposes only and should not be construed as tax, legal, or financial advice. Tax laws and regulations are complex, vary by jurisdiction, and are subject to change. The examples provided are hypothetical and for illustrative purposes only. Individual circumstances vary significantly, and what applies to one person may not apply to another. Settel provides information and planning tools but does not provide tax, legal, or financial advice. We strongly recommend consulting with qualified tax professionals, accountants, or legal advisors who are familiar with the specific tax laws and treaties relevant to your situation before making any decisions or taking any actions based on this information.

Related Topics: Multi-jurisdiction tax calculator, cross-border tax accuracy, Statutory Residence Test, Double Taxation Agreements, tax residency ties, UK FIG regime, expat tax planning

Tags: #MultiJurisdictionTax #TaxCalculator #CrossBorderTax #ThreeCountryProblem #SRT #DTA #ExpatTax #TaxPlanning