Master Wealth Tracking Procedure for Expats Across Countries

Managing finances across the United States, United Kingdom, India, and United Arab Emirates introduces a tangle of accounts, currencies, and tax rules few platforms can handle smoothly. As an expat or digital nomad, keeping tabs on shifting FX rates, forgotten accounts, and inconsistent government data standards is a real headache. This guide breaks down practical steps for gathering your financial records, connecting global accounts, and mastering cross-border tax settings so you can create a clear, unified view of your wealth and obligations.

Table of Contents

- Step 1: Gather Financial Data Across Jurisdictions

- Step 2: Connect Accounts and Assets to a Unified Platform

- Step 3: Configure Multi-Currency and Tax Settings

- Step 4: Review and Validate Consolidated Wealth Overview

- Step 5: Optimize Cross-Border Tax Obligations

Key Takeaways

| Primary Insights | Detailed Explanation |

|---|---|

| 1. Thoroughly collect financial data | Gather comprehensive financial documents from every country where you have accounts or assets to build an accurate financial overview. |

| 2. Utilize a unified financial platform | Integrate all collected financial information into a single platform to streamline tracking and minimize errors across jurisdictions. |

| 3. Configure tax settings accurately | Ensure correct residency status and tax settings to avoid overpaying taxes or missing important deadlines. |

| 4. Regularly validate financial information | Consistently review and reconcile your financial data with actual statements to catch errors before they lead to tax issues. |

| 5. Optimize your tax obligations legally | Identify treaty benefits and foreign tax credits, and strategically plan your finances to minimize overall tax burdens without evasion. |

Step 1: Gather Financial Data Across Jurisdictions

You're about to collect the raw materials for your complete financial picture. This step sets the foundation for everything that follows, so getting it right matters more than getting it fast.

Start by listing every country where you currently hold financial accounts, earn income, or own assets. For most expats, this includes your home country, your current country of residence, and potentially others where you have ongoing investments or property.

Here's what you need to gather from each jurisdiction:

- Bank statements from checking and savings accounts (last 12 months)

- Investment account statements including stocks, bonds, and mutual funds

- Cryptocurrency exchange accounts and wallet information

- Property deeds and mortgage documents

- Pension or retirement account statements

- Insurance policies with cash value

- Any rental income documentation or business entity records

The reality is that cross-government data exchange remains inconsistent across borders, which means you'll need to pull this information manually rather than relying on automatic syncing between countries. Each jurisdiction maintains separate financial records, and automating retrieval across them isn't yet standardized.

![]()

Create a simple spreadsheet with three columns: Country, Account Type, and Last Updated. This becomes your master checklist. Mark off each account as you collect statements, noting the date so you know when to refresh the data.

Pay special attention to currency conversion. Don't try to convert everything right now, just gather statements in their original currencies. You'll normalize them later with current exchange rates, which is crucial since FX rates shift daily and affect your tax liability calculations.

Many expats miss accounts opened years ago and forgotten. Scan your email for old bank confirmations, brokerage statements, or property purchase documents. If you've moved frequently, you likely have dormant accounts scattered across multiple countries.

Collect 12 months of statements from each account, not just the most recent month. Tax authorities often request historical data, and year-over-year comparisons help you spot patterns in your income and asset movements.

Pro tip: Create a dedicated folder in your email or cloud storage labeled by country and account type, then set calendar reminders to download fresh statements on the same day each month. This prevents the scramble when you need documents quickly and ensures consistency across your tracking.

Here's a quick comparison of key challenges and practical solutions for managing cross-jurisdictional finances:

| Challenge | Impact on Expats | Practical Solution |

|---|---|---|

| Inconsistent data standards | Difficult to automate collection | Create manual checklists, keep records in original format |

| Forgotten accounts | Potential compliance issues | Search old emails, reconcile dormant accounts regularly |

| Currency fluctuation | Alters net worth and tax calculation | Normalize data using daily rates, postpone conversions until review |

| Tax treaty complexity | Risk of overpaying or missing deadlines | Document residency and treaty benefits clearly in platform |

Step 2: Connect Accounts and Assets to a Unified Platform

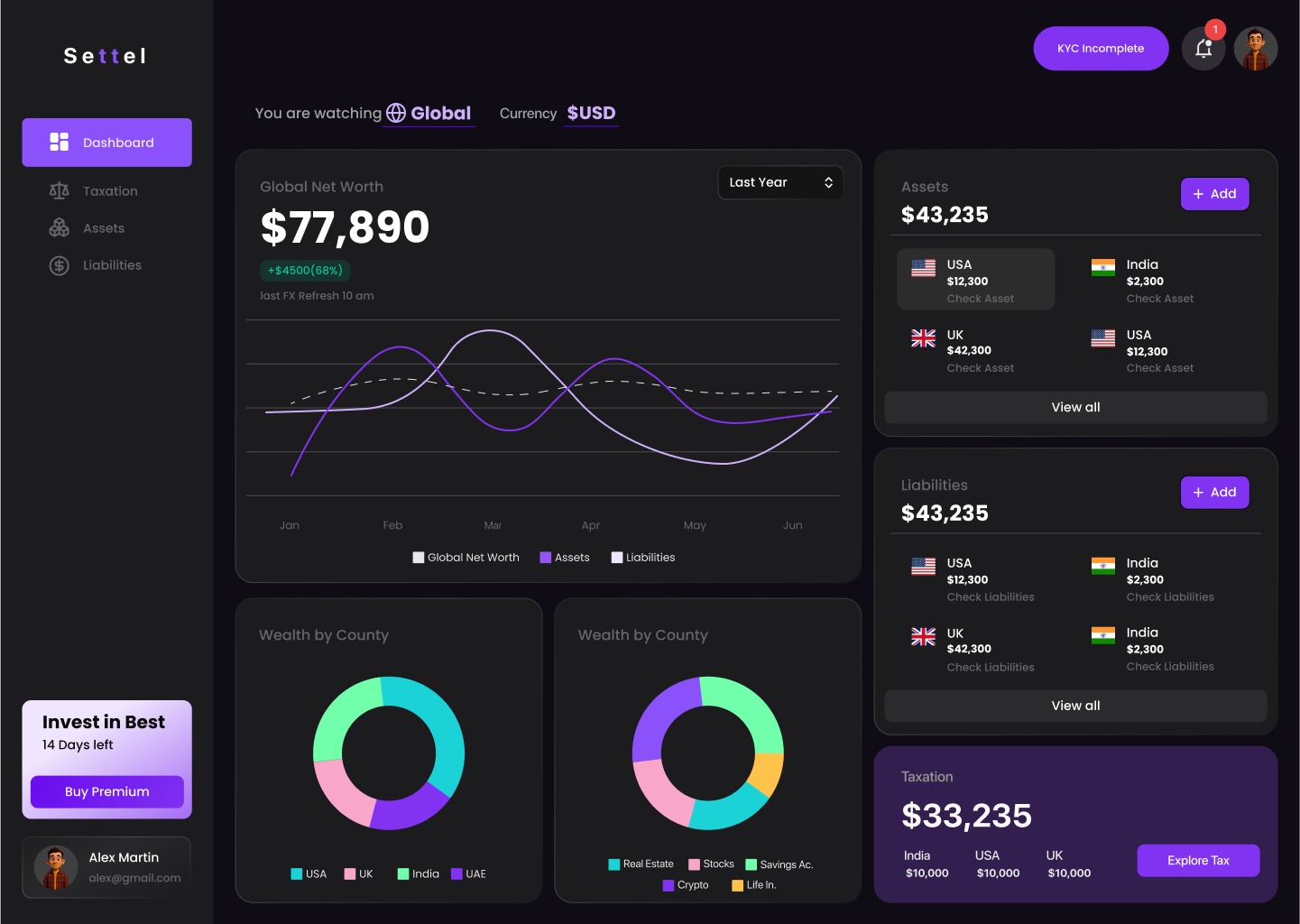

Now that you've gathered your financial documents, it's time to bring them into one place. A unified platform eliminates the mental overhead of tracking accounts across multiple countries and currencies.

Start by choosing a platform that supports multi-currency tracking and integrates with financial institutions across your jurisdictions. Look for one that handles bank accounts, investments, crypto, and property valuations in a single dashboard.

The connection process typically follows these steps:

- Create your account and set your base currency (usually USD, GBP, EUR, or INR for expats)

- Add each financial account manually or through secure integrations with your banks

- Upload supporting documents like property deeds and investment certificates

- Verify account balances match your actual statements

- Set up regular sync schedules for live account updates

Open banking and cross-border data aggregation have evolved significantly, making it easier to connect accounts securely across borders without sharing passwords. Many platforms now use tokenization and encrypted APIs rather than storing login credentials.

When connecting accounts, prioritize security. Use two-factor authentication on every account, and verify that your platform encrypts data both in transit and at rest. This matters especially when dealing with sensitive financial information across multiple countries.

Don't rush this step. Verify each connection by comparing the platform balance to your actual bank statement. A mismatch signals a syncing issue that needs fixing before you proceed to tax calculations.

Crypto holdings require special attention since exchanges vary by country and some don't offer direct API connections. You may need to manually upload transaction histories or connect through specialized crypto portfolio trackers that feed into your main platform.

A unified platform becomes unreliable if you don't keep it current. Stale data leads to incorrect tax estimates and missed reporting deadlines across your jurisdictions.

Pro tip: Connect your accounts in batches by country rather than all at once, testing each jurisdiction's integrations before moving to the next. This approach helps you identify any regional-specific connection issues early and avoid the frustration of troubleshooting multiple failures simultaneously.

Step 3: Configure Multi-Currency and Tax Settings

Your platform now holds all your financial data, but it won't be useful until you configure it to reflect your actual tax situation. This step translates raw numbers into actionable intelligence about what you owe across your jurisdictions.

Start by selecting your base currency. This is the currency in which you'll view your total net worth. Most expats choose their home country currency or USD for consistency, though some prefer the currency of their country of residence.

Next, set up your residency status for each jurisdiction. Your residency classification determines which taxes apply to you and which tax treaties protect you from double taxation. This is where complexity enters quickly.

Here's what to configure:

- Your residency status in each country (resident, non-resident, or uncertain)

- Your tax residency rules under that country's domestic laws

- Any applicable double tax treaties between your countries

- Your foreign tax credit eligibility and limitations

- Reporting thresholds that trigger mandatory disclosures

Understanding how to manage wealth across multiple jurisdictions requires accurate configuration of your tax residency and treaty benefits. Misconfiguring these settings leads to either overpaying taxes or missing critical filing deadlines.

Link each account in your platform to its corresponding tax jurisdiction. A UK bank account should be tagged as United Kingdom income, a US brokerage account as United States investment income, and so on. This categorization is essential because different countries tax different income types differently.

Configure currency conversion settings to use daily average rates or your platform's preferred methodology. This consistency matters when tax authorities ask how you calculated foreign currency gains or losses during the tax year.

Many platforms allow you to set up tax scenario modeling. If you're uncertain whether you qualify as a tax resident in a particular country, create scenarios for both outcomes. This helps you understand your exposure and plan accordingly.

Residency status determines everything in your tax picture. Get this wrong and every calculation downstream becomes unreliable.

Pro tip: If your residency status is uncertain in any jurisdiction, document the factors that support your classification (physical presence, property ownership, family ties, economic interests) in your platform's notes section. When tax authorities question your status, you'll have a clear record of your reasoning.

Step 4: Review and Validate Consolidated Wealth Overview

You've built your wealth dashboard and configured your tax settings. Now comes the critical work of validating that everything reflects reality accurately.

Start by running a full account reconciliation. Compare your platform totals against your actual bank statements, investment account summaries, and property valuations. Line by line. This isn't exciting work, but mismatches here cascade into tax miscalculations later.

Check these specific items:

- Bank account balances match your latest statements

- Investment positions reflect current holdings, not stale data

- Currency conversions use current exchange rates

- Property valuations are reasonable and documented

- Cryptocurrency quantities match your exchange wallets

- Loan amounts and mortgage balances are accurate

Look for missing accounts. Did you forget that old savings account from five years ago? An inherited property in your home country? A forgotten pension from a previous employer? Expats commonly overlook accounts they haven't actively used recently.

Validate your income categorization. Each income stream should be tagged to the correct country and income type. Employment income from the United States shouldn't be labeled as United Kingdom investment income. This categorization drives everything else in your tax calculations.

Review your tax treaty settings. If you benefit from a Double Taxation Agreement between your countries, verify it's configured correctly in your platform. These treaties often have specific rules about which country gets primary taxing rights over certain income types.

Perodic review and validation of your consolidated wealth overview ensures your numbers stay aligned with your actual circumstances as your life changes. Job changes, moves between countries, new acquisitions, and inheritance all shift your financial picture.

Don't validate once and forget. Set a quarterly review schedule to catch changes before tax season arrives. Major life events like relocation or significant asset purchases should trigger immediate reconciliation.

Compare your platform's total net worth calculation against your own manual calculation. If they don't match, dig into the variance. Is it a currency conversion difference? A missing account? An incorrect balance entry?

Validation catches errors early when they're cheap to fix. Discovering account mismatches during a tax audit is far more expensive.

Pro tip: Export your consolidated wealth overview as a PDF snapshot each quarter and store it securely. This creates a timestamped record of your financial position that can protect you if tax authorities later question the accuracy of your reported assets or wealth changes.

Step 5: Optimize Cross-Border Tax Obligations

Now that you understand what you owe, it's time to strategically reduce that burden. Tax optimization isn't tax evasion, it's legitimate planning within the rules your countries provide.

Start by identifying your tax treaty benefits. Most countries with significant expat populations have Double Taxation Agreements that prevent you from being taxed twice on the same income. These treaties specify which country has the right to tax certain types of income first.

Here's what to review in your specific treaties:

- Primary taxing rights for employment income

- Investment income and dividend treatment

- Capital gains rules and exemptions

- Pension and retirement account treatment

- Real property taxation protocols

- Tie-breaker rules if you qualify as resident in multiple countries

Understanding international tax treaties and legal frameworks helps you navigate obligations strategically and identify where you can legitimately reduce your overall tax burden across jurisdictions.

Next, consider foreign tax credit optimization. If you've already paid taxes in one country, many countries allow you to credit those payments against your tax liability there. However, the rules vary significantly. Some countries allow dollar-for-dollar credits, while others cap the credit or calculate it differently.

Explore income sourcing strategies. Where you earned income matters. Passive income generated in a low-tax jurisdiction may face different treatment than employment income earned in a high-tax jurisdiction. This doesn't mean hiding income, but rather understanding the tax implications of different income types.

Review your charitable giving approach. If you donate to charity in one country but have tax obligations in another, you need to understand which country allows deductions for your donations. Some countries don't recognize foreign charity deductions at all.

Consider timing of income and expenses. If you're transitioning tax residency between countries, the year of transition matters. Accelerating income into one year or deferring it to another can meaningfully reduce your total tax across both jurisdictions.

Below is an overview of common income types and their typical cross-border tax treatment:

| Income Type | Jurisdiction Tax Treatment | Optimization Tip |

|---|---|---|

| Employment | Usually taxed where earned | Review treaty for primary taxing rights |

| Investment | Varies by country/asset | Tag correctly and apply credits as allowed |

| Pension/Retirement | Taxed in payout country, often treaty protected | Check treaty exemptions or credits |

| Rental Property | Taxed in source country | Document ownership and local reporting |

| Crypto Gains | Treatment varies widely | Use accurate records, anticipate manual filings |

Documentation matters here. Keep records showing how you calculated your foreign tax credits, which treaty provisions you relied on, and why you structured transactions the way you did.

Treaty benefits don't apply automatically. You typically must claim them explicitly on your tax returns or file special forms to prove your eligibility.

Pro tip: Before making major financial decisions like selling significant assets or changing residency, run the tax calculation both ways in your platform. Seeing the difference between scenarios often reveals thousands of dollars in savings available through timing or structuring adjustments.

Take Control of Your Cross-Border Wealth with Settel

Managing finances across multiple countries is challenging. From gathering financial data to configuring tax residency and optimizing tax obligations, the process can quickly become overwhelming. This article highlights the key pain points expats face like tracking multi-currency accounts, understanding residency statuses, and navigating complex tax treaties.

Settel was designed specifically to solve these exact problems. Our platform offers a multi-currency wealth dashboard that consolidates your bank accounts, investments, crypto, and property in one place. It uses live FX rates to give you a clear, unified view of your total net worth. Plus, our Smart Tax Engine analyzes residency, income types, double taxation agreements, and foreign tax credits to deliver accurate, personalized tax obligations across the US, UK, India, and UAE.

Stop wasting weekends hunting down statements or guessing your tax responsibilities. Visit Settel now to join the waitlist and start organizing your wealth with confidence. Learn more about how we handle multi-currency wealth dashboards and tax optimization for expats so you never miss a deadline or overpay again.

Frequently Asked Questions

How do I gather financial data across different countries?

Start by listing all the countries where you hold financial accounts or own assets. Collect 12 months of statements for each account, including bank statements, investment accounts, and any income documentation.

What information should I include in my wealth tracking spreadsheet?

Create a spreadsheet with three columns: Country, Account Type, and Last Updated. This will help you maintain a clear overview of your financial accounts and track when you last refreshed your data.

How can I connect my accounts to a unified platform?

Choose a platform that supports multi-currency tracking, then manually add each financial account and upload supporting documents. Verify that each connection matches your actual bank statements for accuracy.

What settings do I need to configure for my multi-currency and tax obligations?

Select your base currency, set your residency status in each jurisdiction, and link each account to its corresponding tax jurisdiction. This ensures that your platform accurately reflects your overall tax obligations and prevents miscalculations.

How often should I validate my consolidated wealth overview?

You should conduct a full account reconciliation quarterly to ensure accuracy in your financial data. Regular validation helps identify any discrepancies early, preventing issues during tax season.

What strategies can I use to optimize my cross-border tax obligations?

Review your tax treaties for benefits, such as avoiding double taxation. Consider timing income and expenses strategically to minimize your overall tax burden across jurisdictions.