India tax for NRIs in 2026: obligations and strategies

Many NRIs mistakenly believe all their global income is taxable in India, leading to confusion and potential compliance errors. The reality is far more nuanced. Residential status determines tax scope: only income earned or received in India faces taxation for NRIs, while foreign earnings remain exempt. This guide clarifies Indian tax rules specific to NRIs for 2026, covering residency definitions, taxable income categories, filing requirements, and optimization strategies. You'll learn how to navigate the 182-day rule, choose between tax regimes, and leverage Double Taxation Avoidance Agreements to minimize your liability legally.

Table of Contents

- Understanding NRI Tax Residency Rules In India

- What Income Is Taxable For NRIs In India?

- NRI Income Tax Slabs, Filing Requirements, And Forms

- Tax Planning Strategies And Compliance Tips For NRIs

- Discover Expert NRI Wealth Management And Tax Solutions

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Income scope | Only income earned or received in India is taxable for NRIs, foreign income is exempt |

| Residency impact | Your residential status determines tax liability scope and available exemptions |

| Regime choice | NRIs can choose between old and new tax regimes with different rate structures and deductions |

| Filing mandate | ITR filing is mandatory above INR 2.5 lakh Indian income using specific forms like ITR-2 or ITR-3 |

| Tax optimization | Strategic planning using DTAA benefits, regime selection, and RNOR status can reduce tax burden |

Understanding NRI tax residency rules in India

Your tax residency status in India is the foundation of your entire tax obligation. The Indian Income Tax Act defines three categories: Non-Resident Indian (NRI), Resident but Not Ordinarily Resident (RNOR), and Resident. These classifications hinge on the number of days you spend in India during a financial year and your income sources.

The primary rule is straightforward: you're an NRI if you stay less than 182 days in the financial year. However, there's a secondary rule that catches many off guard. If you spend fewer than 60 days in India during the current financial year AND fewer than 365 days over the previous four years, you also qualify as an NRI.

The 60-day threshold has critical exceptions. If you're a Person of Indian Origin (PIO) or an Indian citizen working abroad who visits India, the threshold increases to 182 days. But here's where it gets tricky: if your Indian income exceeds INR 15 lakh, the 60-day rule tightens to just 120 days. This 120-day trap has caught countless high-earning NRIs by surprise, converting them unexpectedly to resident status.

RNOR status offers a middle ground for returning NRIs. You qualify as RNOR if you've been a non-resident in at least two of the previous ten years or stayed in India for 729 days or fewer during the preceding seven years. The benefit? Your foreign income and assets remain exempt from Indian taxation even as a resident, giving you breathing room to restructure your finances.

Tracking your stay duration isn't optional anymore. Immigration records, flight bookings, and hotel stays all leave digital trails. A single miscalculation can shift your status and expand your tax liability dramatically. The difference between 119 days and 121 days in India could mean the difference between zero tax on foreign income and full taxation.

Pro Tip: Use a digital diary or dedicated travel tracking app to log every entry and exit from India with timestamps. Set alerts at 100 days to review your remaining buffer and avoid crossing critical thresholds unintentionally.

What income is taxable for NRIs in India?

Understanding which income streams trigger Indian tax liability eliminates guesswork and prevents overpayment. NRIs are taxed only on income that accrues, arises, or is received in India. Everything else falls outside Indian tax jurisdiction.

Taxable income categories include salary for services rendered in India, even if paid abroad. Rental income from Indian property is fully taxable regardless of where you receive the payment. Capital gains from selling Indian assets like stocks, mutual funds, or real estate trigger tax obligations. Interest earned on Non-Resident Ordinary (NRO) accounts is taxable, unlike NRE accounts.

Non-taxable income provides significant relief. Your foreign salary for work performed outside India is completely exempt. Capital gains from foreign assets remain untouched by Indian tax authorities. Interest on NRE and FCNR accounts is exempt, making these accounts attractive for parking repatriated funds.

Here's a practical example: Suppose you earn a salary of USD 80,000 in the US, receive INR 3 lakh in rental income from a Mumbai apartment, and earn INR 50,000 interest on an NRO account. Your taxable Indian income is only INR 3.5 lakh (rental plus NRO interest). The US salary remains exempt.

| Income Type | Taxable Status | Example |

|---|---|---|

| Foreign salary | Exempt | USD salary for work in US |

| Indian salary | Taxable | Compensation for India services |

| Indian rental income | Taxable | Rent from Delhi property |

| Indian capital gains | Taxable | Sale of Mumbai flat |

| NRO interest | Taxable | Savings account interest |

| NRE/FCNR interest | Exempt | Fixed deposit returns |

| Foreign investments | Exempt | US stock dividends |

Tax Deducted at Source (TDS) applies to most payments to NRIs at higher rates than residents. Rental income faces 31.2% TDS, while interest and professional fees see rates between 20% and 30%. This upfront deduction means you often overpay taxes, making ITR filing essential to claim refunds. Understanding TDS obligations helps manage cash flow and ensures you recover excess withholding.

Pro Tip: Maintain a dedicated folder with bank statements, rental agreements, and sale deeds that clearly establish the source and location of each income stream. This documentation becomes critical when claiming exemptions or responding to tax notices.

NRI income tax slabs, filing requirements, and forms

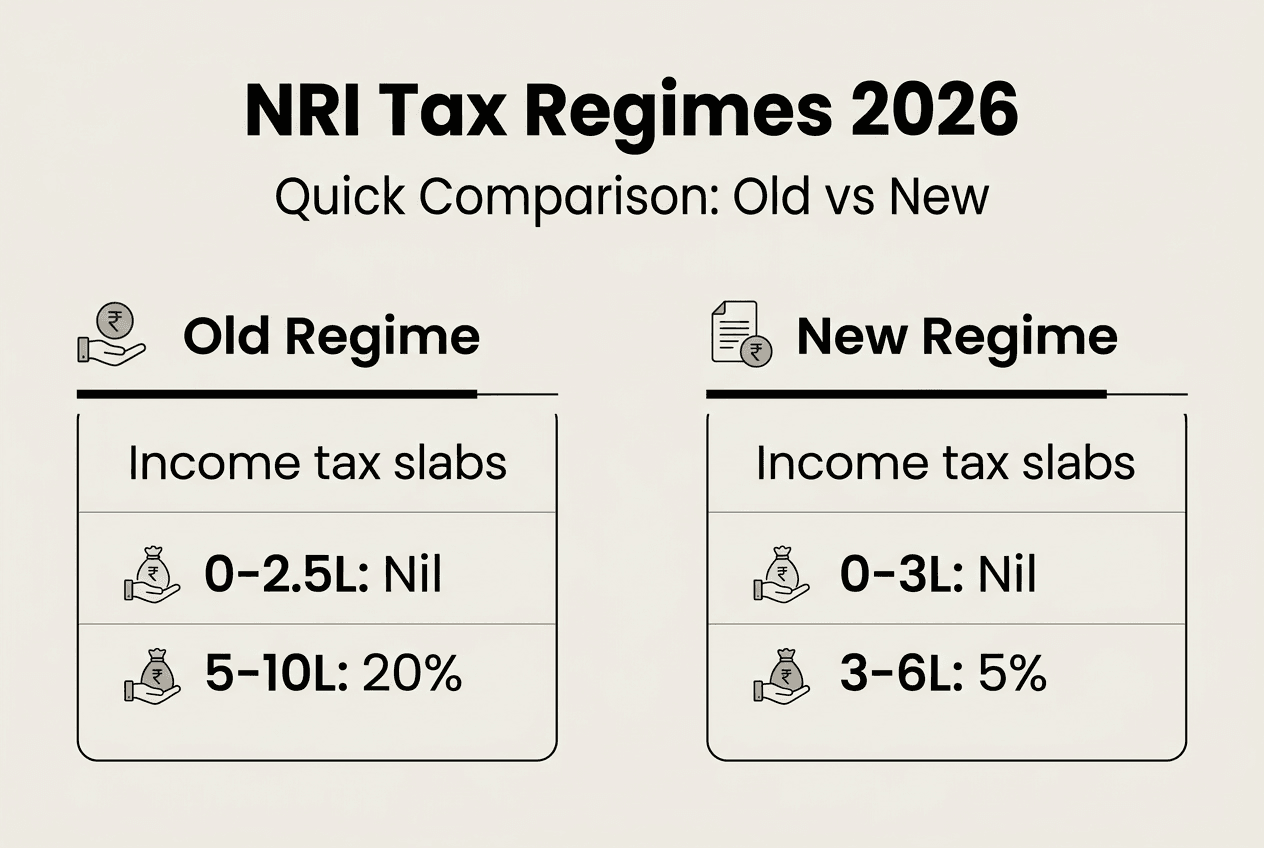

NRIs face the same tax rate structure as Indian residents, but with crucial differences in regime choice and available deductions. You can opt for either the old tax regime with higher rates but generous deductions, or the new regime with lower rates but minimal deductions.

Under the old regime, tax slabs range from zero to 30% based on income brackets. Income up to INR 2.5 lakh is tax-free, INR 2.5 to 5 lakh is taxed at 5%, INR 5 to 10 lakh at 20%, and above INR 10 lakh at 30%. Surcharges kick in at higher income levels: 10% for income between INR 50 lakh and INR 1 crore, 15% between INR 1 crore and INR 2 crore, 25% between INR 2 crore and INR 5 crore, and 37% above INR 5 crore. A 4% health and education cess applies to the total tax plus surcharge.

The new regime offers lower rates: zero up to INR 3 lakh, 5% from INR 3 to 6 lakh, 10% from INR 6 to 9 lakh, 15% from INR 9 to 12 lakh, 20% from INR 12 to 15 lakh, and 30% above INR 15 lakh. However, you forfeit most deductions like Section 80C, home loan interest, and HRA. One critical difference: NRIs cannot claim the INR 12,500 rebate under Section 87A available to residents.

| Tax Regime | Income Slabs | Key Features |

|---|---|---|

| Old Regime | 0-2.5L: Nil; 2.5-5L: 5%; 5-10L: 20%; 10L+: 30% | Allows 80C, home loan, HRA deductions |

| New Regime | 0-3L: Nil; 3-6L: 5%; 6-9L: 10%; 9-12L: 15%; 12-15L: 20%; 15L+: 30% | Lower rates, minimal deductions, no 87A rebate |

Filing requirements are mandatory if your Indian income exceeds INR 2.5 lakh or if you want to claim TDS refunds. Even with lower income, filing establishes a clean compliance record and facilitates future financial transactions in India. The standard deadline is July 31 for most NRIs, extending to August 31 if your accounts require audit.

NRIs must use specific ITR forms based on income sources. ITR-1 (Sahaj) is off-limits for NRIs. Most use ITR-2 for salary, rental, and capital gains income without business income. If you have business or professional income, ITR-3 is mandatory. ITR-4 (Sugam) is also not available for NRIs.

Here's your filing roadmap:

- Gather all income documents: Form 16, rental agreements, capital gains statements, and bank interest certificates

- Download Form 26AS from the income tax portal to verify TDS credits

- Choose between old and new tax regimes based on your deduction eligibility

- Fill the appropriate ITR form (ITR-2 or ITR-3) online or through a tax professional

- Verify the filed return using Aadhaar OTP, net banking, or by sending a signed physical copy

- Track refund status if TDS exceeded actual tax liability

TDS rates for NRIs are significantly higher under Section 195, often 20% to 30% on interest, royalties, and technical fees. This creates a cash flow burden but also means most NRIs receive refunds after filing. The key is filing promptly to accelerate refund processing. Leveraging global tax treaties through DTAA provisions can reduce TDS at source if you submit the right certificates upfront.

Tax planning strategies and compliance tips for NRIs

Optimizing your NRI tax position requires proactive planning, not reactive filing. The difference between strategic tax management and passive compliance can save lakhs annually while keeping you fully compliant.

Start with meticulous day counting. Track your India stay to avoid unintended residency, especially if your Indian income exceeds INR 15 lakh where the 120-day threshold applies. Set calendar alerts at 90 days and 110 days to review your position. If you're approaching limits, consider postponing non-essential India trips to the next financial year.

Double Taxation Avoidance Agreements (DTAA) between India and your country of residence offer powerful relief. However, benefits aren't automatic. You must proactively submit a Tax Residency Certificate (TRC) from your country of residence and Form 10F to Indian payers before they process payments. TRC and Form 10F submission enables lower TDS rates under treaty provisions, improving immediate cash flow.

Regime selection demands careful analysis. The old regime works better for high deductions like home loan interest exceeding INR 2 lakh or significant Section 80C investments. If you're claiming minimal deductions, the new regime's lower rates often win. Run the numbers both ways before committing, as you can switch regimes annually.

RNOR status provides a golden window for returning NRIs. Leverage RNOR for tax-free foreign asset liquidation during the transition years. Sell foreign stocks, close overseas accounts, and repatriate funds while your foreign income remains exempt. Once you become a full resident, these same transactions trigger Indian tax.

Key tax-saving approaches include:

- Timing capital gains to utilize exemptions and lower rates

- Maximizing Section 80C through PPF, ELSS, or life insurance if using old regime

- Claiming home loan interest deductions up to INR 2 lakh under Section 24

- Structuring rental income to claim standard deduction and actual expenses

- Using NRE/FCNR accounts for repatriated savings to earn tax-free interest

Compliance tips prevent costly errors. File your ITR by the deadline even if you owe zero tax to maintain a clean record. Use the correct ITR form based on your income sources. Keep digital and physical copies of all supporting documents for seven years. Update your address and contact details on the income tax portal to receive notices promptly.

Pro Tip: Consult tax advisors who specialize in NRI taxation and have experience with your specific country of residence. Generic tax advice often misses jurisdiction-specific nuances in DTAA application that can save significant amounts.

"The biggest mistake NRIs make is treating Indian tax filing as a once-a-year scramble. Proactive DTAA certificate submission, regime selection analysis, and stay tracking throughout the year prevent surprises and optimize outcomes. Tax planning is a continuous process, not an annual event." - Senior Tax Consultant specializing in NRI taxation

Discover expert NRI wealth management and tax solutions

Managing NRI taxes and cross-border finances doesn't have to feel like navigating a maze blindfolded. The complexity of tracking income across jurisdictions, applying treaty benefits, and optimizing tax positions demands specialized expertise and tools designed for globally mobile professionals.

Settel specializes in simplifying multi-country wealth and tax management for NRIs and expats. Our platform handles tax planning across India, US, UK, and UAE, monitors compliance deadlines, and provides personalized strategies to minimize your global tax burden. Whether you need help choosing the right tax regime, claiming DTAA benefits, or understanding residency implications, our multi-jurisdictional advisory takes the guesswork out of compliance. Stop wrestling with spreadsheets and fragmented advice. Explore how Settel streamlines your global wealth management and keeps you compliant across borders.

Frequently asked questions

What is the definition of an NRI for Indian tax purposes?

An NRI is an individual who resides in India for less than 182 days in a financial year or meets the secondary test of staying fewer than 60 days in the current year and fewer than 365 days over the previous four years. Exceptions apply for Indian citizens working abroad and PIOs, where the 60-day threshold increases to 182 days. If your Indian income exceeds INR 15 lakh, the threshold tightens to 120 days, potentially converting you to resident status.

Which incomes are exempt from tax for NRIs in India?

Foreign-sourced income including salary earned abroad, capital gains from foreign assets, and interest on NRE and FCNR accounts are completely exempt from Indian taxation for NRIs. Only income that accrues, arises, or is received in India faces tax liability. This includes Indian salary, rental income from Indian property, capital gains from Indian assets, and interest on NRO accounts.

Do NRIs have to file income tax returns in India every year?

NRIs with Indian income exceeding INR 2.5 lakh must file an Income Tax Return annually. Filing is also mandatory if you want to claim refunds for excess TDS deducted during the year. Even with income below the threshold, filing establishes a compliance record and facilitates banking and investment transactions in India. The deadline is typically July 31, extending to August 31 for cases requiring audit.

What are the tax filing deadlines for NRIs in India?

Tax returns for NRIs are generally due by July 31 for the financial year ending March 31. If your accounts require audit under income tax provisions, the deadline extends to August 31. Early filing accelerates refund processing if you've had excess TDS deducted. Missing deadlines triggers late filing fees of INR 5,000 (reduced to INR 1,000 if income is below INR 5 lakh) and potential interest on unpaid taxes.

How can NRIs claim relief under Double Taxation Avoidance Agreements?

NRIs must submit a Tax Residency Certificate (TRC) from their country of residence and Form 10F to Indian payers before income payments are processed. Proactive TRC and Form 10F submission enables lower TDS rates under applicable DTAA provisions instead of standard higher rates. You can also claim foreign tax credits when filing your ITR to offset Indian tax against taxes paid abroad on the same income, preventing double taxation.

Recommended

- Global Tax Reporting: Avoid 75% Penalties in 2026 | Settel Blog | Settel

- Expat Asset Protection: 5 Strategies with 100% Compliance | Settel Blog | Settel

- 3 Types of Global Tax Treaties: 90% of Nations Use DTAAs | Settel Blog | Settel

- Settel Expats: Wealth Management & Tax for Expats in US, UK, UAE, India